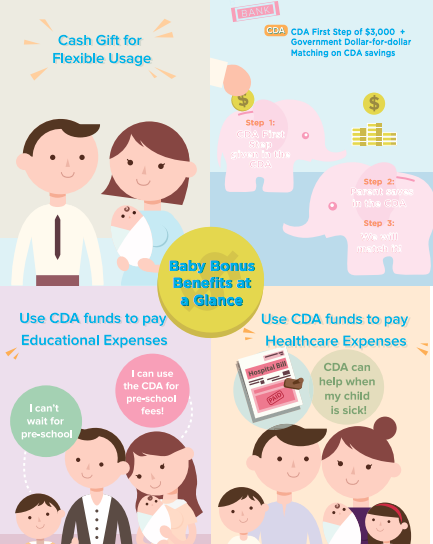

Getting pregnant, delivering a child and raising them sure isn’t cheap in Singapore. To help encourage more couples to have babies, our government has given various incentives including a Baby Bonus cash gift ($8k each for your first two kids, and $10k for the third onwards), a $3000 Child Development Account (CDA) First Step Grant, and dollar-to-dollar matching if you contribute and save up in your child’s CDA.

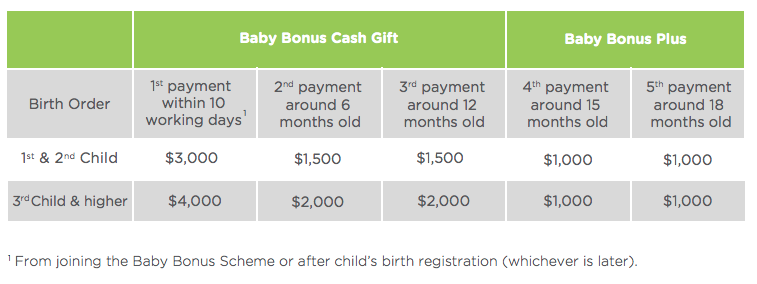

Please pay attention to the last column of “Total Baby Bonus Benefits”, which tells you the maximum amount you’ll be able to get from the government. But beyond that, I’m also here to share with you how I intend to boost this even further than what’s stated on the MSF Baby Bonus Booklet Brochure here!

What do I need to do to get my money?

1. Register at MSF’s website here with your SingPass. You can do this either up to 2 months before your expected delivery date, or after your child has been born.

2. Wait for the government to deposit the Baby Bonus cash gift into your bank account (either yours or your spouse) according to this schedule:

3. Open a Child Development Account for your newborn (after he/she is born) in order to get the cash grant of $3,000.

4. Deposit money into your child’s CDA to enjoy the dollar-to-dollar matching benefits.

|

| Image credits: MSF |

What can CDA funds be used for?

You can use it to pay for your child’s healthcare expenses, insurance, pharmaceutical purchases (Watson’s and Guardian) and even education or childcare centre fees. For a list of approved institutions, you may refer to MSF’s website here.

Can I withdraw CDA funds?

Unfortunately, CDA funds are restricted to certain approved usage only. When your child turns 12, the CDA is closed and any unused balance funds will be transferred to their Post-Secondary Education Account (PSEA), which can be used to pay for their school fees and other educational activities.

How much will I get?

If you don’t do anything other than registering for the Baby Bonus Scheme and opening a CDA for your newborn, you’ll get:

- $11,000 for your first and second child each

- $13,000 for your third child onwards

How can I get MORE?

However, to really maximise what you get, here’s what I intend to do:

- Top up to the maximum cap of $3,000 in CDA to get the full dollar-to-dollar matching right from the start ($9k for your third and fourth child, and $15k for your fifth).

- This will allow the magic of compound interest to set in early!

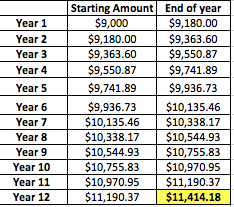

Since I’m delivering my firstborn next month, I intend to do this during my confinement period (in December) so that we’ll start off with the full $9,000 in our son’s CDA right away. At 2% interest p.a., this will give us about $11,400 by the time he turns 12 (assuming no withdrawals are made).

Contrast this to if we take our own sweet time and only put in $500 every year from the second year onwards, until we hit the maximum cap in the 8th year.

As you can see, to get the maximum possible interest on the CDA, it’ll be worth making that cash top-up right from the start rather than later on, over the years (provided you have the cashflow and liquidity). Parents having their third, fourth or fifth child onwards can benefit from even more interest by topping up CDA earlier rather than later, since the dollar-to-dollar matching cap is even higher at $9k and $15k each!

Of course, if you have other higher-yielding bank accounts to park your funds in (eg. DBS Multiplier, UOB One, OCBC 360, etc) that give you more than 2% p.a. interest, then those might be a better option to consider as well. However, my husband and I will be separating our son’s funds from that of our own, so we’ll be putting the full $3,000 in his CDA in December.

Should I put in even more?

No, I wouldn’t personally put in beyond the maximum cap to enjoy the government’s dollar-for-dollar matching grant, because at the end of the day, the CDA funds are more restrictive and less liquid i.e. you can’t simply withdraw them easily for cash, nor are you entitled to spend them as you wish (except at approved institutions mentioned above).

Which is the best CDA account to open?

We can only choose from DBS, OCBC and UOB – these are the only approved banks to offer CDA at this moment. Here’s how they stack up:

|

UOB CDA |

OCBC CDA |

POSB Smiley CDA |

| Interest Rate |

2% (no limit) |

2% on first $36,000 and 0.05% after |

2% (no limit) |

| Merchant Tie-Ups |

No |

Yes |

Yes |

| Medical Spend Rebate |

No |

No |

3% rebate with Passion POSB Debit Card for services at hospital, medical and dental clinics |

| Junior Savings Account |

No |

Up to 0.8% p.a. on Mighty Savers Account |

0.05% on POSBKids Account |

Current Promo

(as of 2018) |

None |

Receive $108 with purchase of Maternity Insurance and/or $100 for Endowment Plan (min. premiums >$3k) |

Free SIA Infant ticket on economy class

(till Jan 2019) |

After reviewing the respective offerings by the three local banks, we’ve decided to open with POSB Smiley CDA because:

1. The rebate for medical, dental and hospital expenses is a key draw.

OCBC used to offer this, but has unfortunately since removed this privilege as of October 2018.

2. OCBC Mighty Savers is a common reason why some parents open a OCBC CDA, but both accounts can be mutually exclusive.

Up to 0.8% p.a. on your child’s own saving account is indeed a compelling draw, but I found out that there’s no need for it to be tied to a OCBC CDA in order for your child to enjoy the same benefit. However, you must have a OCBC CDA account in order to meet the requirements to get 0.4% p.a. interest, otherwise, you’ll only be able to qualify for up to 0.4% p.a.

In the meantime, I’ll also be waiting for the other banks to see if they’ll up their game and offer more enticing child saving accounts. It won’t be too late for me to open one later on when my baby is older.

3. POSB’s CDA merchant tie-ups and promotions are more useful.

I reviewed the different merchant tie-ups between OCBC and POSB, and felt that POSB’s partners are more relevant because I get to utilize RedMart’s offers, and get child essentials through GAIA, BabyNatureCo, VitaKids and even Pororo Park entry, etc. You might want to review the different merchant tie-ups for yourself and decide which ones would be more useful to you as well.

4. The current promotion by OCBC is quite redundant vs. POSB’s.

On the other hand, the free SIA infant flight ticket will come in handy as we’re already planning a family trip abroad next year to attend my best friend’s wedding (yes, we’ll be bringing baby!). Instead of having to pay a percentage of adult flight tickets + taxes + surcharges, we can get one free on economy class for our son under the current POSB CDA promo instead.

Which CDA account will you be opening for your newborn, and why? Let me know in the comments below if you chose anything other than POSB!

SGD deposits are insured up to S$75k by SDIC.

Note: This is NOT a sponsored post.

With love,

Budget Babe

2 comments

Congrats and all the best for your upcoming delivery! My wife is due in 3 months so these articles have been really useful, especially your research on cord blood banking !

that's great to hear! haha oh man the cord blood banking research really took me a long time to gather, and quite a few months before we made our decision on which bank to go with. glad you and your wife have found these useful! a few more coming up right before I pop 😛

Comments are closed.