As an investor, some of the biggest frustrations we face are generally:

- Refusing to sell when our investment thesis changes – often holding on in “hopes” that things will get better

- Failing to buy when price fell to an all-time low

- Buying before we did sufficient “homework” on the company – especially when it involves missing out on a crucial piece of information that changes the entire thesis

- Missing out on a good gem

No wonder people say that the biggest obstacle in investing can sometimes be ourselves – our own emotions.

One of my biggest regrets to date was having missed out on Dutech Holdings. When I started investing last year, it was one of the first stocks I examined which I was convinced would be a good buy. Back then, the share price was hovering between $0.28 and $0.30.

In recent weeks, the market has been paying more attention to Dutech, thanks to CIMB initiating a “BUY” rating on this counter. I thus revisited my investment thesis which I first wrote in March 2015 and parked away in the deep abyss of my computer folders. Sources of updated information, figures, charts and certain images are rightfully credited to CIMB, Thumbtack Investor and from Dutech’s own annual reports.

What I liked about Dutech

For those who are unfamiliar with the company, Dutech claims to be the largest safe manufacturer in Asia while serving plenty of global customers. Their key business can be divided into 2 segments – High Security (ATMs, gun safes, commercial safes, cash handling systems and gaming terminals) and Business Solutions (manufacturing intelligent terminals and electro-mechanical equipment to semi-conductor, printing and automotive industries).

The security business is a niche market and recession-proof. With increased AML regulations, a rise in prolific ATM-hacking incidents and increased security spending (in light of terrorism) across countries, there was a clear growth story for Dutech. The only question would be whether they would be able to successfully capitalize on these growth opportunities and translate that into actual, tangible sales.

|

| Credits: CIMB |

Clients: Diebold, Wincor Nixdorf (which then got acquired by Diebold afterwards), Hitachi, Winchester, Liberty Safe & Security Products, Scientific Games, Costco, Bauhaus, etc. Mostly global customers who are pretty big and reputable names in the market.

Their competitive moat: Dutech states that they are one of the few global players who are both UL and CEN certified, with low-cost production bases in China and Germany.

Forex exposure: This is actually beneficial to Dutech, as their sales are mostly in USD while costs are in RMB (China). Thus, lower RMB and higher USD works in their favour.

Costs: Steel is a key raw material for Dutech’s products. With lower steel prices, this should translate into higher gross margins for Dutech.

Management Know-How: It would be an understatement to say that much of Dutech’s growth has been largely in part to Dr. Johnny Liu, who formerly held leadership roles in Thermal Dynamics USA and Murray Inc. He also studied engineering in the US, where he achieved a PhD. I did a background check and also found that he had six patents to his name, which is another good sign of his capability and innovation. Dr. Liu is still young so it is unlikely for him to retire anytime soon, thus there’s no need to worry about succession plans yet.

Key Shareholders: In addition to Dr. Liu, Dutech’s COO Mr. Winson Chen and Sales Director Ms. Jessica Shi Yi also own a significant portion of Dutech’s shares. Management’s combined shareholdings is 60%. Their largest external shareholder is Mr. Robert Stone, who has been growing his stake via the open market every year, and has openly announced his liking for this counter.

It is always a good sign when management is a significant shareholder, as it demonstrates both confidence in their company as well as ensuring greater alignment to shareholder interest. (They stand to benefit as a shareholder as well.) This is always an important consideration, as there are plenty of companies who are good businesses but not necessarily aligned to shareholder interests.

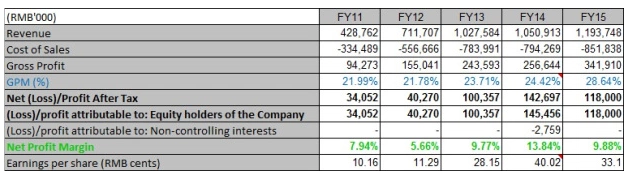

Financial Highlights

Revenue and net profits have been rising steadily, with respectable high gross profit margins of over 20% on average (this figure continues to climb each year).

Their biggest contributor to revenue comes from the High Security segment (94% in 2013 vs. 65% of total revenue in 2015). Keep an eye on that 600% growth from their Business Solutions as a testimonial to how their acquisitions are indeed paying off.

|

| Credit: Thumbtack Investor, who has beautifully consolidated these. |

When the operating environment is so attractive, it usually attracts the entrance of new competitors. Globally, their key competitor is Gunnebo AB, which is the world’s largest high security equipment producer, listed on the Stockholm Stock Exchange with a market cap of over 3 billion and PE ratio 17. As Dutech is headquartered in Shanghai, I also looked at safe producers in China – Shanghai Golden Door Security Equipment, Shenzhen Yihua Computer, Huizhou Delipu, Wuxi Bam Precision Metal Works, Shanghai Baolei and Wuxi Yongchuang. However, out of this list, Tri Star has the most CEN-certified products and is much larger in size globally.

|

| Credit: Thumbtack Investor. Not showing my own chart because it’s super messy with tons of comments in every other cell. |

The company is also in a good position to pay off its short-term debt without any risk of bankruptcy. What is even more impressive is that Dutech can actually pay off all of its current liabilities with their cash pile alone, as they have been consistently growing their free cash flow (FCF) every year.

Growth stock or a stagnant company?

Dutech’s growth in recent years has largely been inorganic i.e. through acquiring companies that would add value to their business expansions.

In late 2011, Dutech acquired their competitor Format, a loss-making company, and managed to turn it around into a profitable business within 3 years by shifting some of Format’s manufacturing productions to China. Format also enabled Dutech to expand its sales in Europe.

In late 2014, they acquired Deutsche Mechatronics GmbH, which gave them entry into the intelligent terminals market, although the company is loss-making at the moment. Note that Dutech also needs to pay off the remaining RMB 3.9 million in 2019 for this acquisition.

In December 2015, they spent close to 2.5 million euros on acquiring and investing into Krauth, which produces auto-ticketing machines and money changes. The results of this recent acquisition has yet to be fully translated onto its balance sheet, which could be a potential catalyst for improved financials in the near future.

What I was uncertain about Dutech

First of all, the biggest hurdle about Dutech is that it is an S-chip. (S-chips are Chinese businesses listed in SGX but with Chinese management at the helm.) Talk to older, more experienced investors and many will tell you about the sector’s accounting scandals and trading suspensions not too long ago. This has tainted and put off many investors from parking their cash into S-chips. You can read more about them at China Stock Fraud Blog and here.

Furthermore, Dutech is so low profile that it doesn’t even have its own website; instead, you have to view it through TriStar Group. Their website is difficult to navigate, and there is no consolidated IR section for you to easily retrieve information at one shot. This was a concern to me, but at the same time, I liked that its low profile would mean it’ll be missing from the radar of many investors.

I also prefer value stocks which give out dividends so that I get paid while waiting for the market to eventually reprice the company to a fair value. However, Dutech has no formal dividend policy, and no dividends were paid out in FY12 and FY13. As cash is needed to fund growth through acquisitions, I was unsure if dividends would potentially get slashed for good while management retained cash for such opportunities.

Diebold, Wincor Nixdorf and Liberty are among Dutech’s biggest customers. If any sales are lost to another supplier, Dutech’s earnings will be greatly impaired. Although Dutech talks about their strong customer relationships in their annual report, there is no guarantee of customer retention as companies generally tend to look out for lower-cost suppliers where possible.

With the rise of digital payments such as Alipay, cash might become less preferred, which may then lead to fewer ATM withdrawals and therefore longer replacement cycles. This will negatively affect Dutech’s revenues, although it would just be one portion out of their diversified business segments.

Dutech matched my criteria of a deep-value stock

In value investing, we seek to identify under-valued companies and wait for its value to eventually be recognized by the market. In an efficient market (“EMT Theory”) where information flow is perfect and investors make rational decisions, it holds that the stock price of a company at any time will always reflect its fair value (as a bare minimum). Unfortunately, we all know that markets are hardly efficient in real life, especially in the short-term. Failure of being fully-informed, media coverage and human psychology are just some of the many reasons why share prices end up being under or over-valued for many companies.

Unfortunately, when you venture into deep-value contrarian investing, it is hard to be 100% confident since you’re essentially going against herd mentality. There is also the very real risk of falling for a value trap if you don’t know what you’re doing. Imagine how I felt as a beginner investor – due to my inexperience, I wasn’t sure if I had correctly unearthed a true value gem, or whether I was looking at a value trap that other investors knew about and rightfully avoided…therefore justifying its low price. My favourite line, when it comes to describing my weaknesses, is that I don’t know what I don’t know.

So I consulted a few folks whom I considered to be financially-savvy, as experienced “experts”. 2 of my trusted aides told me that they would avoid it by a yardstick. The main reason? It was a China company. Just look at the problems that have surfaced in other Chinese companies – corruption, fraud, financial engineering in their numbers, etc.

Thus I sadly saved my investment thesis, which I had documented down after hours and hours of research, and parked it away into the deep abyss of my folders while waving goodbye to the stock.

If only I hadn’t let myself be swayed – then today I would be sitting on 66% gains.

Is Dutech Holdings a good Buy now?

When I first spotted Dutech, I had only the FY14 annual report as my base, where it was trading at PE 3.6 and PB 0.4. At such valuations, it was definitely a deep-value stock. I just wasn’t sure if it was truly a diamond or just a shining rock.

Today, as of FY15, its NAVPS (net asset value per share) is 43 cents. At today’s price of 49 cents, the PE ratio is 6.8 and PB 1.1. Trailing dividend yield is 2.2% (remember that even this is not guaranteed).

What caused Dutech’s stock price to shoot up so drastically? Largely thanks to CIMB analyst coverage, which has increased public awareness of this stock counter. My regret was that I hesitated for too long and did not end up buying while I had the chance.

The PE valuation still makes Dutech an attractive buy, if you believe in its growth story, but at today’s prices, I shall give it a miss because I refuse to buy anything above book value in today’s economic climate.

Now excuse me while I go mope over the one that got away.

18 comments

It's always easy in hindsight.

That's why it's important to have a plan. If your plan is to buy deep value stocks, perhaps you could buy a basket of 10-20 of them so that your portfolio won't suffer as much if some of them turns out to be duds.

The thing about S-chips is that people fall to the composition fallacy, thinking that all S-chips are risky. This presents good opportunity for those who do their research. I believe 1 thing that reduces the chance of a fraud is insider buying/ownership. For example, Dr Johnny's share transactions in 2013.

So being more "experienced" now, if you find another S-chip like Dutech, what would you do?

This comment has been removed by the author.

Another problem of value investors is that they usually sell too earlier, and P/B is not necessarily always a good indication of value. There are perfect value stocks such as Vicom/Boustead which will never trade below book. Whether it justifies to trade above book depends on how good the ROE is. Dutech is riding on the same tailwinds (cheap raw material price, favourable FX) as Riverstone last time (which proved to be a multibagger).

My biggest obstacle is myself! Haha. I try to be more focused though on the stocks I pick so it is also easier to monitor moving forwards.

I spotted a few more but have yet to confirm their potential. If I find another Dutech-like counter, I will definitely put in some money this time! Not a core holding, but at least 8%

On insider buying and ownership though, there's a good number of companies with that happening. So while I agree with you that it's a good sign, it cannot be taken alone at face value. I know of folks who blindly chase -.-

Agree,my under PB ratio is not simply applied across all the stocks I'm looking at either. Riverstone rode on more favourable tailwinds back then imo, Dutech today still needs to contend with rise of digital cashless payments which is still uncertain, although granted their business is diversified enough not to be too negatively impacted by these headwinds. Right now I think Dutech is at fair value, so I'll pass, but if it drops below fair value I might consider again depending on the size of my warchest (which is sadly small for a young investor)

Hi Budget Babe,

Lovely write up. It first caught my eye in January this year when CIMB gave a non-rating write up. It has indeed shot up before I get to dip my feet into it. However, the same happened to me for Best World.

I think I will still give it a shot if it hovers between 37-40 cents.

Rgds,

Heartland Boy

ROE 14-15%, P/BV only 1.0x, with earnings growth.

Well, don't regret again 🙂

That feel when you realize you missed out on a gem…

Well organized analysis! I am amazed that you didn't go into details on the business solution sections,which Dutech is focusing a lot of energy right now and wants to make it a significant part of business. Auto vending machine, ticket machine, gaming machine etc are growing faster in China right now. The potential demand of this seciton in China is huge. Dutech could enjoy double digit growth in this section for several years…

I don't like to look at "potential" until they materialise… those plans and acquisitions still remain a big question mark at this point, although management has certainly shown themselves to be capable so far. Maybe I'll do part 2 of this once we have more visibility in the coming quarters 🙂

The recent false rally has made my heart ache too!

If it should go down further, I might reconsider. But at this point, prices are fairly valued in my opinion. For those who are seeing this as a growth play, it might not be too late to enter (to each their own), but in my eyes this has run its course of a value stock given what they have today. Of course, with more in the pipeline for Dutech they may still have room to run…

If you look at the revenue and profit from business solution section, they are starting to materialize. Dutech's subsidiary tristar is already the top 5 supplier of SZZT electronics. with the acquisition of DTMT and Krauth, they are building up their R&D and mfg capability to produce their own intelligent machine. I searched from Jiangsu Provence regulation website, which indicated the government also approved Tristar's proposal of building up the product line to enable annual capacity of 30,000 smart-end terminals in end of 2014. I believe this section will be the growth pillar going forward 🙂

Interesting! I'd love to chat more. Drop me an email? My email contact is sgbudgetbarbie [at] gmail {dot} com!

I would like to suggest that you pick the ultimate Forex broker – AvaTrade.

Comments are closed.