If you have ever bought shares through a broker and wondered, “Wait, why aren’t my shares showing in CDP?”, you are not alone.

For many Singapore investors, CDP has always felt like the default. You buy SGX-listed securities, the securities appear in your CDP account, dividends come into your linked bank account, AGM notices arrive, and everything feels reassuringly direct.

But in recent years, more investors — especially those using brokers with low or zero commissions — have started holding their securities through broker custody accounts instead.

That has created a fair bit of confusion.

Are the securities really mine? Is custody less safe? Will I still receive dividends? Can I attend AGMs? What happens if there is a rights issue?

These are not silly questions. In fact, they are exactly the questions every investor should ask before deciding where to hold their investments.

Background

Before we dive in, here’s the key context: Singapore investors can hold SGX-listed securities either through their own CDP account or through a broker custody account.

The confusion usually starts because both allow you to invest, but the way your securities are held — and how dividends, corporate actions and AGM matters are handled — can differ.

With SGX supporting greater adoption of broker custody accounts, it is time for every investor to understand what each setup comes with, and the pros and cons of each.

Generous sign-up gifts are nice, but they should not be the sole reason you use to decide where to hold your investment portfolio, especially if you intend to be consistent and grow your portfolio capital over time.

In this article, I’ll break down

- how both structures work,

- what rights and processes may differ among each broker type, and

- the key questions you should ask before deciding which account setup suits you better.

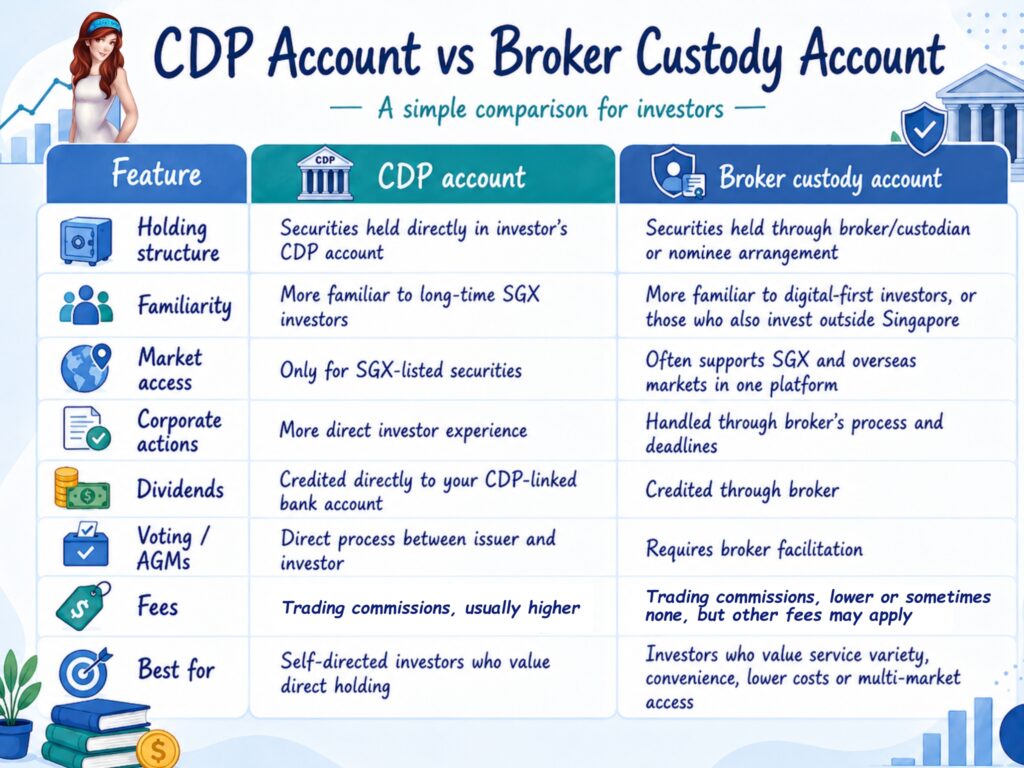

The difference between a CDP account and a broker custody account

For those who may not be familiar, a CDP account generally means your SGX-listed securities are held directly in your own name with CDP. But even with CDP, you still need a brokerage account to buy and sell securities.

With a broker custody account, your securities are held through the broker’s custody or nominee structure. In such cases, CDP records the broker’s name and the broker in turn records your beneficial interest in the holdings. The operational handling of dividends, corporate actions and account servicing goes through the broker.

It is worth noting since the CDP system was introduced in 1987, many Singapore investors have gotten used to owning shares in their own names. However, this has been limited to the Singapore markets.

If you own any assets in overseas markets, that has always been under a custody arrangement – regardless of whether you go through your bank or broker to invest.

Neither structure is superior. But they are not identical either — and the differences can matter when you receive dividends, act on a rights issue, attend an AGM or transfer your holdings later.

Broker custody accounts offer convenience and lower costs – especially if you invest across markets

When I first started investing in the early 2010s, there were very few brokers for me to choose from. Back then, the only custodian account was offered by Standard Chartered Bank, where transaction fees were $10 per counter instead of the usual $25.

Today, custodian accounts are increasingly common and charge transaction fees as low as $1.

This also tends to be the global practice across other overseas markets, where there is no such thing as a centralised system like CDP.

And since investors today often buy stocks across multiple markets – Singapore, US, Hong Kong, ETFs, options, etc – these are where custody accounts are the default and sometimes the only option.

Investors choosing to use custody accounts are able to view their allocations by asset class and geography within a single app. They may even be able to take advantage of online tools to analyse their portfolio’s risk and performance, or seek and receive customised advice from their brokers on portfolio optimisation and corporate actions.

In contrast, those who choose to use CDP accounts will have to maintain separate accounts for their Singapore vs. overseas securities.

But…do you still own your securities?

In a custody arrangement, investors are the beneficial owners of the securities, while the broker/custodian or nominee holds the securities on behalf of clients. The operational relationship is different from CDP, but that does not mean the broker can simply treat your securities as its own.

MAS regulations (under the Securities and Futures Act) require separation of investors’ holdings from brokers’ holdings. Brokers must also keep a record of which investor owns what.

In terms of safety, then, the more important question is not: “CDP or custody?” Rather, it should be: “How do I safeguard my wealth?”

After all, a well-regulated structure will not help much if you voluntarily hand your login details to a scammer pretending to be customer support! At the end of the day, safety also boils down to:

- Use licensed and regulated brokers.

- Read account terms and risk disclosures.

- Enable 2FA and strong passwords.

- Watch out for phishing and impersonation scams.

- Keep your own records of holdings.

- Avoid transferring money to personal accounts or suspicious third-party accounts.

The “cheap broker” may not always be cheapest once you include all fees

Traditionally, it costs more to transact through CDP-linked broker accounts. I personally pay $25 per transaction to my bank brokerage each time I wish to buy and have my SGX-listed securities show up in my own CDP account.

On the other hand, custody accounts charge lower or sometimes no trading commissions. The real difference shows up when dividends, rights issues and AGMs happen, as they may impose custody, transfer, corporate action, foreign exchange or dividend handling fees.

For investors who already buy and sell stocks in other markets, this fee-for-service model is probably familiar and may even be more attractive. For others, a higher upfront fee may be preferred.

To decide what works best for you, you should compare not just the headline commission rate, but also the full cost of owning, receiving income, acting on corporate actions and transferring your securities if you ever want to.

At the same time, you need to understand that dividends, rights issues, AGMs and voting will not work the same way.

For CDP accounts, corporate actions and dividend handling may feel more direct and familiar. I get my dividends paid directly into my bank account (which is linked to CDP), but if you used a custody broker, then the dividends will show up in your brokerage fund or wallet held there. Attending AGMs is also more straightforward since I do not have to contact my broker to get the right to attend – the invitation letter simply arrives straight in my inbox.

For broker custody accounts, the broker will need to process instructions, collect responses from clients, and aggregate submissions and meet custodian or market deadlines.

Example: Let’s say a company announces a rights issue. If your shares are in CDP, you may receive the instructions directly through the usual CDP-related channels. But if your shares are held through a custody broker, your broker may set an earlier internal deadline because it needs time to collect client instructions and submit them before the market deadline.

Miss the broker’s deadline, and you may lose the chance to act — even if the official market deadline has not passed yet.

Here are more examples:

- Dividend crediting dates may differ.

- Rights issue subscription deadlines may be earlier via custody brokers.

- AGM registration and voting require making requests through your broker.

- Scrip dividends, preferential offerings and voluntary corporate actions may have broker-specific instructions.

- Service fees may apply for certain corporate actions.

As every broker differs, I would encourage you to contact your respective brokers to understand their timelines, service fees and any account-related questions.

CDP vs. Custodian: Which account type is better for you?

There is no right or wrong, and no one account type is better than the other.

To simplify it for you, CDP may be preferable if:

- You value direct holding and/or your familiarity with the CDP structure.

- You use multiple brokers for SGX-listed securities.

- You prefer receiving information through CDP-related processes.

- You want a structure that feels more straightforward for local securities.

- You are no longer an active investor and are mostly just collecting dividends from your portfolio.

On the other hand, broker custody may suit you better if:

- You invest across multiple markets.

- You value having one place to view your holdings across markets.

- You want access to a wider range of broker services such as portfolio-specific trading advice and margin financing.

- You prefer lower-cost digital platforms.

- You actively trade or rebalance.

You don’t have to settle for either one. A mix may suit you if you are transitioning gradually and want to test the process first, or if you would like flexibility to use custody accounts for active portfolio management while maintaining your CDP for long-term holdings.

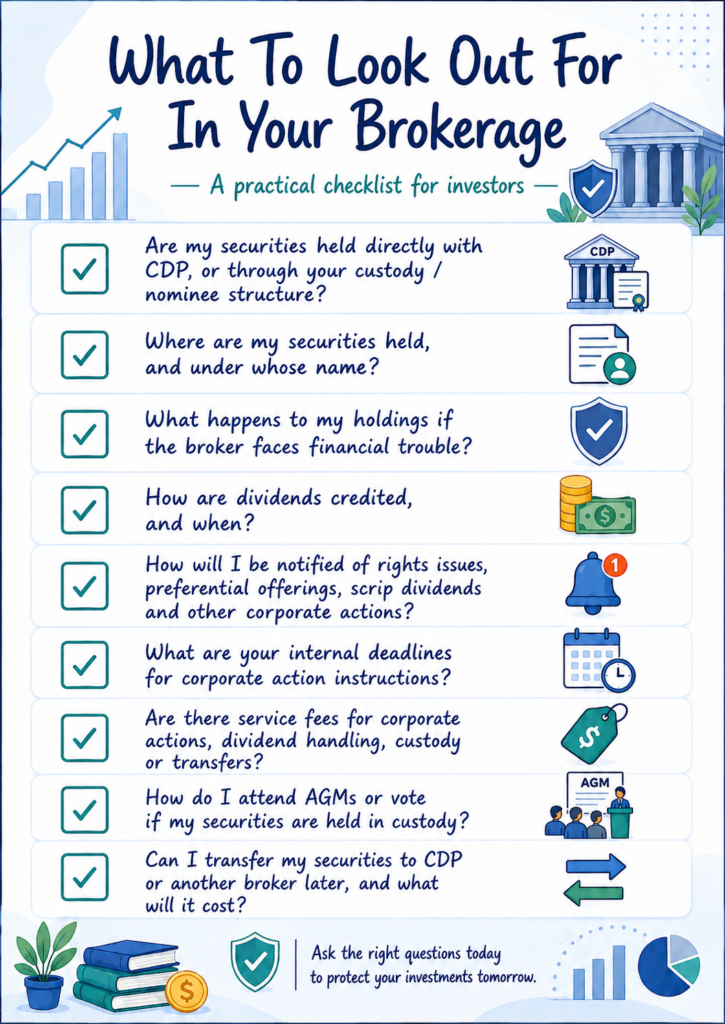

If you choose custody accounts, I’ve compiled a checklist of questions that you can go through with your brokerage so that you fully understand what you’re signing up for:

As Warren Buffett says, risk comes from not knowing what you’re doing.

In this era where share ownership is now entirely digital and no physical stock certificates are being issued anymore, this applies to knowing how our chosen broker works and operates as well.

So regardless of whether you opted for a CDP-linked broker or one that holds your portfolio assets under a custody or nominee structure, it is worth asking yourself these questions:

- Where are my securities held, and under whose name?

- What happens to my holdings if the broker faces financial trouble?

- How are dividends credited, and when?

- How will I be notified of rights issues, preferential offerings, scrip dividends and other corporate actions?

- What are your internal deadlines for corporate action instructions?

- Are there service fees for corporate actions, dividend handling, custody or transfers?

- How do I attend AGMs or vote if my securities are held in custody?

- Can I transfer my securities to CDP or another broker later, and what will it cost?

My Take

As broker custody accounts become more common, investors need to understand what they are signing up for before something important happens — not only when there is a rights issue, dividend delay, AGM registration issue or transfer request.

I don’t think retail investors need to be afraid of broker custody accounts just because their securities do not appear in CDP. But I also don’t think we should blindly choose the cheapest broker without first understanding its custody arrangement, corporate action process, fee schedule and transfer rules.

At the end of the day, CDP and broker custody accounts are not “good” or “bad”. They are simply different ways of holding investments, each with its own trade-offs.

For some investors, CDP will continue to make sense because it is familiar, direct and easy to understand for Singapore-listed holdings. On the other hand, broker custody accounts may be more practical for those who invest across multiple markets, prefer digital platforms, or want potentially lower transaction costs.

The key is to choose with your eyes open.

Before deciding where to hold your portfolio, make sure you understand how your chosen account works — including fees, dividend handling, corporate actions, AGM access, voting rights and transfer processes.

Because when it comes to investing, what matters is that you actually understand how your chosen account works — including fees, corporate actions, dividend handling, AGM access and transfer processes — before deciding where to hold your portfolio.

Disclosure: This is a sponsored post brought to you in partnership with the Securities Investors Association (Singapore). You can also read their thoughts on this topic here, which was published in The Straits Times earlier this year.