Is Standard Chartered’s Unlimited$aver worth signing up for?

|

| Video screencap from Standard Chartered |

As the product teaser goes,

“Been scoring 1.5% cashback with your Standard Chartered Unlimited Cashback Credit Card? Now you can unlock our highest cashback* of 5% with Unlimited$aver.”

I’ve been seeing so many ads for this product lately that it piqued my interest, and so I took a closer look at it. My conclusion? Nay.

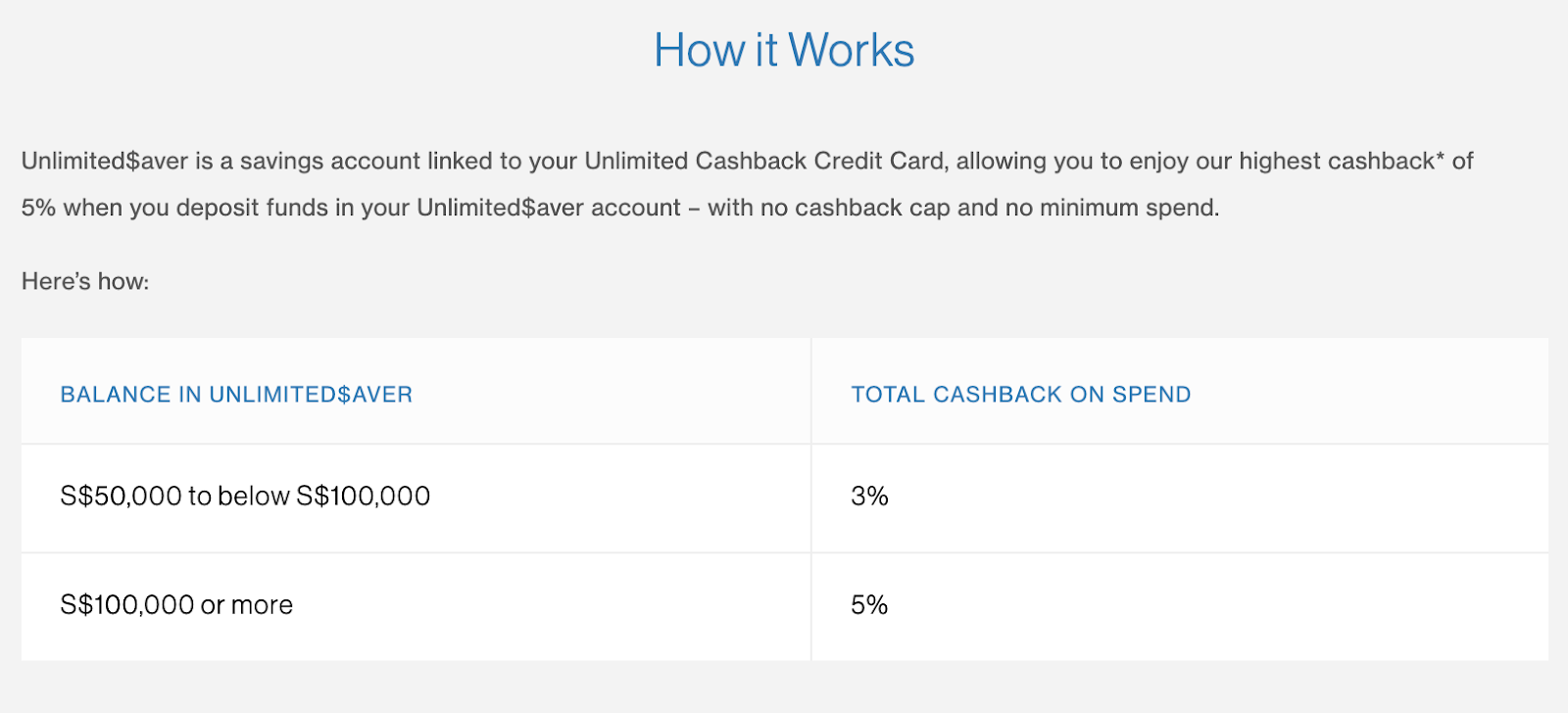

How Does It Work?

At first glance, it definitely seems promising enough – 5% cashback is among the highest in the cashback market right now. Unfortunately, once you start to compare among the other options you could go for with the same amount of funds, the attractiveness of SC’s promotion starts to fade away.

Let’s first look at how SC’s Unlimited$aver seems compelling:

With $100k of funds in your Unlimited$aver bank account, you’re immediately eligible to earn 5% cashback on all your credit card spend. And even if you don’t have a 6-figure lump sum to deposit, anything above $50k will also get you 3% which isn’t shabby at all.

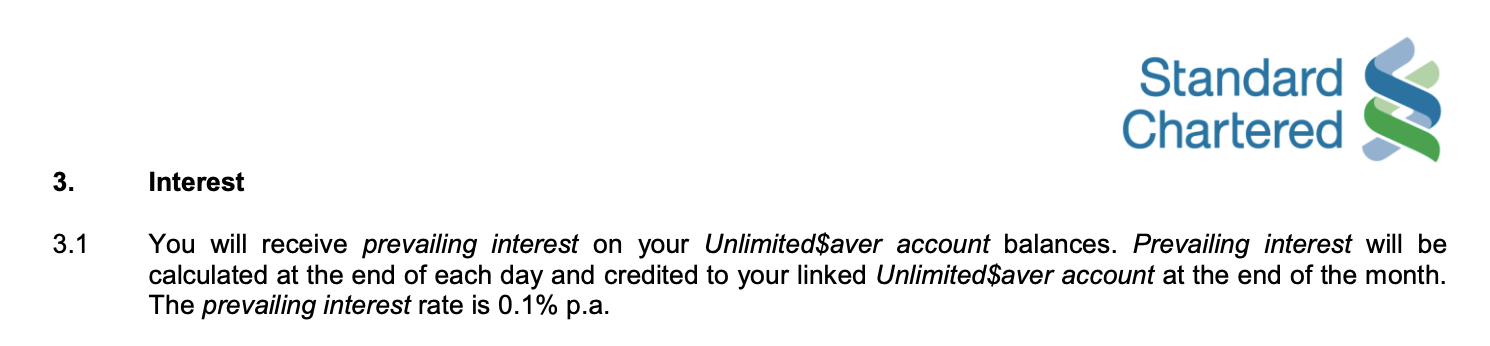

Unfortunately, what you’re getting is a 5% cashback on your credit card spend, and NOT 5% interest on your savings.

The Alternatives

This makes a big difference because if you were to put the same funds into other high-yield savings accounts, you could get so much more:

With $75,000 of deposits and $600 credit card spend each month, you could get:

- $435 on Standard Chartered’s Unlimited$aver + SC Unlimited Cashback Credit Card

- $75 savings interest + $360 cashback

- $1,827 on UOB’s One Account + $200 cashback from UOB One Credit Card

- $600 monthly credit card spend + 3 GIRO transactions

- $1,547 on DBS Multiplier + $456 cashback from DBS Live Fresh Credit Card

- $600 monthly credit card spend + $500 home loan + $100 investments

- Earn $938 interest if only 1 banking transaction eg. salary credit + credit card spend

So is Standard Chartered’s Unlimited$aver Account Bad?

- Are you spending more than $600 on your credit card(s) each month?

- Have you already locked in your salary credit with another bank?

- Do you have more than $50,000 of funds lying around with nowhere else to put them in?

2 comments

I saw this card and I thought it was a bad deal, until I realized that there's no minimum account opening period or fall below fee for the account. This means it's good for those one-off large payments.

Oops, seems like there's a fall below fee but no account closing fee. So you could just deposit, spend, and withdraw the following month.

Comments are closed.