The recent market conditions have reminded me again of what people often say: it really is hard to predict the market.

What if I told you there’s a fail-proof method?

What if I told you this method achieved 8.1% CAGR* in the U.S. market over the past 10 years?

*CAGR = compound annual growth rate

2 weeks ago, the STI Index officially entered bear territory when it dropped to under 2800 points, but stock prices have rallied again and it seems like the index has “recovered”.

There are some who believe that those who didn’t invest then or in the aftermath of Black Monday (both points are highlighted in the chart above) have missed out on the best opportunity to have entered the stock market.

I beg to differ. If you asked me, I find the price increases today irrational, especially given the bleak economic outlook for the next few quarters. So my choice will be to stay on the sidelines and save up cash, as I wait for a better entry point when prices drop again. There really is no hurry.

But at the same time, I was trying to understand more on if there was a way for someone to invest passively without being too bothered by market movements.

My search led me to this seemingly-perfect finding:

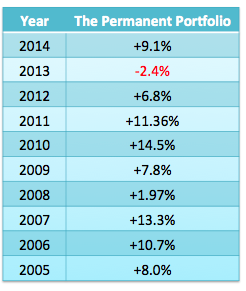

|

| Figures obtained from www.crawlingroad.com which tracks TPP’s performance. |

That’s right! I couldn’t believe it when I first read about the The Permanent Portfolio, a concept designed by Harry Browne to construct a resilient investment portfolio that will preserve one’s money even in economic downturns, yet perform as well (or even better) than a 100% stock market portfolio over the long term.

The book makes a pretty compelling argument for a relatively passive way of investing. For lazier investors (or those who do not really believe in your own abilities to discern and invest in good stocks), this could be a good alternative to build your wealth without too much effort.

How does it work?

The Permanent Portfolio is quite simple. Harry Browne recommends allocating your investment capital to the following assets:

Looking at a longer time horizon, this method achieved a 9.6% CAGR from 1971 to 2012. In other words, if you had invested $10,000 at the beginning, this would have grown to $429,041 over 42 years with no other injections except reinvested returns and rebalancing each year!

Here’s how it performed against the S&P 500:

|

| Credits: Josh Kaufman |

How did this happen? The answer is quite simple.

The beauty of the portfolio lies in how it minimizes and protects against risk through its balancing concept. By dividing your capital equally among the different asset classes, you are diversifying your risk and reaping the results of opposing reactions from each asset class as the market goes through different economic cycles.

Benefit #1: You will no longer need to predict or try to “time” markets.

The portfolio recognizes that financial markets change all the time and invests in assets which counterbalance each other:

Stock Market – does well in periods of prosperity, but poorly in recession, inflation and deflation.

Gold – does well during inflation, but poor during deflation

Government Bonds – generally does well with the lowest possible credit risks, although performance would be relatively poorer during inflation and recession.

Cash – does well in deflation, maintains value in recession, but fares poorly during prosperity inflation.

Benefit #2: You’ll be able to sleep well at night.

A retail investor who has all his capital in the stock market will always be fretting about his counters. There is also the frequent monitoring that one does in order to get peace of mind.

But with this portfolio strategy, regardless of whether the economy is doing well or going down, there is little cause for worry since you know that your portfolio is balancing out against the financial market movements.

Benefit #3: There is little you need to do except to rebalance it annually.

Or quarterly, if you prefer. No more monitoring of your stock counters or market performance!

Benefit #4: You will no longer be swayed by analyst reports.

I generally find analyst reports quite confusing and tend to ignore their buy/sell signals. Also, analysts are not always right all the time. With The Permanent Portfolio strategy, it doesn’t matter what the analysts say – your portfolio will barely be affected since you’re only 25% invested in stocks and the other asset classes balance each other out.

Benefit #5: It really is a no-brainer method.

If you’re skeptical of your own investing abilities, and aren’t too good with doing your own due diligence on stocks, or if you’re simply LAZY, this method is quite straightforward.

This is something I would recommend to people like my parents or older relatives who don’t quite understand how the stock market works, or what to look out for when purchasing a stock counter, or who are always swayed by their brokers!

If you think this sounds promising and would like to learn how to apply it to investing in Singapore, I’ll share more details on the steps you can take locally to make this work for you.

Until then, invest safely!

With love,

Budget Babe

{kind=link}

6 comments

Hi BB,

While I agree that this is a very good and fool proof method, there are just a few more issues to take note of (mainly the liquidity issues of SG market). http://www.bigfatpurse.com/singapore-permanent-portfolio-performance/ has actually simulated a portfolio specific to the SG context. You might want to take a look.

Investingwolf

I have read this book a couple of months ago. Found that the theory sounds workable. Would give it a try!

If you look at the return by bigfatpurse website, this does not seem to work in Singapore context. The return for 4 years is almost 0%.

Or higher 🙂 I'll share this more in a later post.

Remember to do your research first before putting in the money! Do share with me how your portfolio fares 🙂

Hi Investingwolf,

Well said, and thanks for the link! That's why there's a follow-up post in the works 😉

Comments are closed.