Income investing remains attractive to the majority of beginners, as you enjoy regular payouts which you can either spend or reinvest. However, the strategy has become more challenging to execute in recent years as yields decline and capital value of the underlying investment drops. Amidst inflation and rising interest rates, how can investors still apply this strategy to their portfolios?

For many of my friends and I, the first few stocks we bought as a beginner were dividend stocks.

After all, they sounded attractive enough – get paid dividends on a quarterly basis, and see the actual cash show up in your account!

The typical approach for most Singaporean retail income investors involves using a mixture of real estate investment trusts (REITs) and bonds to form their portfolios. A friend of mine became financially independent with this simple strategy, as the dividends from his REITs soon became multiple times more than what his full-time job was paying him, allowing him to quit and declare an early semi-retirement.

But the strategy has not been without challenges in recent years. And with many REITs being sold down due to rising interest rates, and bond yields hardly as attractive as before, it is no wonder that many investors are getting the jitters.

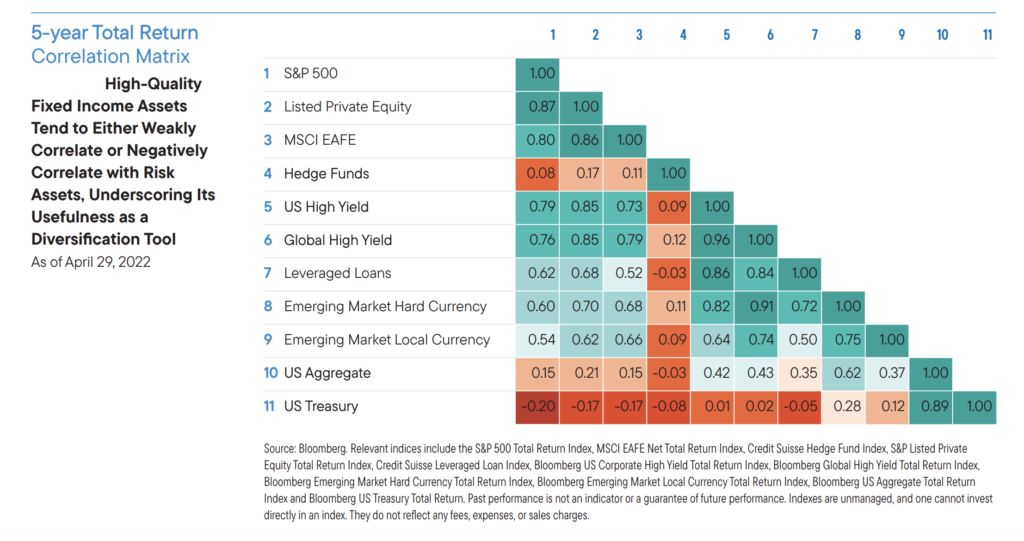

To cope with this, adopting a multi-asset income approach would be a more sensible approach. If you’re willing to cast your net wider to include hybrid instruments, there can be more to explore for yield.

Could bonds be a safer option?

In the past, bonds were a popular way to get yield without worrying about losing your capital.

But the problem is, the returns you can get from bonds are capped on the upside (by the yield of the bond). And in an inflationary environment, the coupons paid out by some bonds may not be enough to keep up.

To tackle this, you can consider adding equities that pay out dividends which can offer potentially higher returns, as your upside is uncapped (due to capital appreciation and higher dividends).

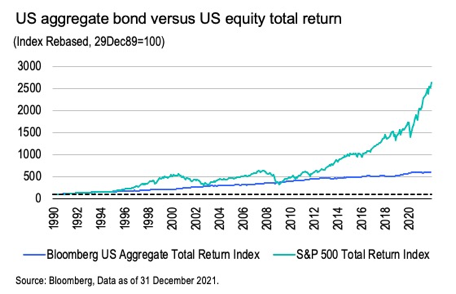

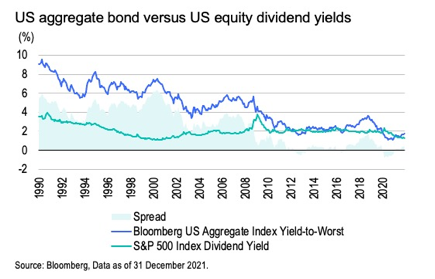

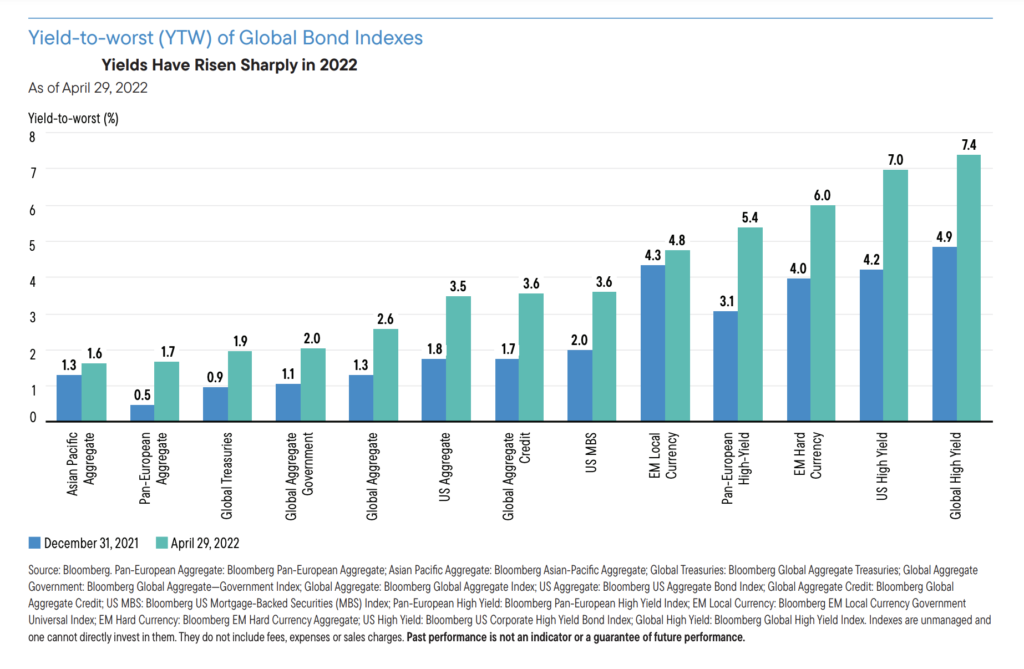

What’s more, in the past, the yields for bonds were typically much higher compared to equities. But this has narrowed in recent times:

Yields on REITs are no longer looking as attractive

With higher interest rates, the yields offered by REITs are now beginning to look less attractive to many investors as compared to less risky tools like fixed income.

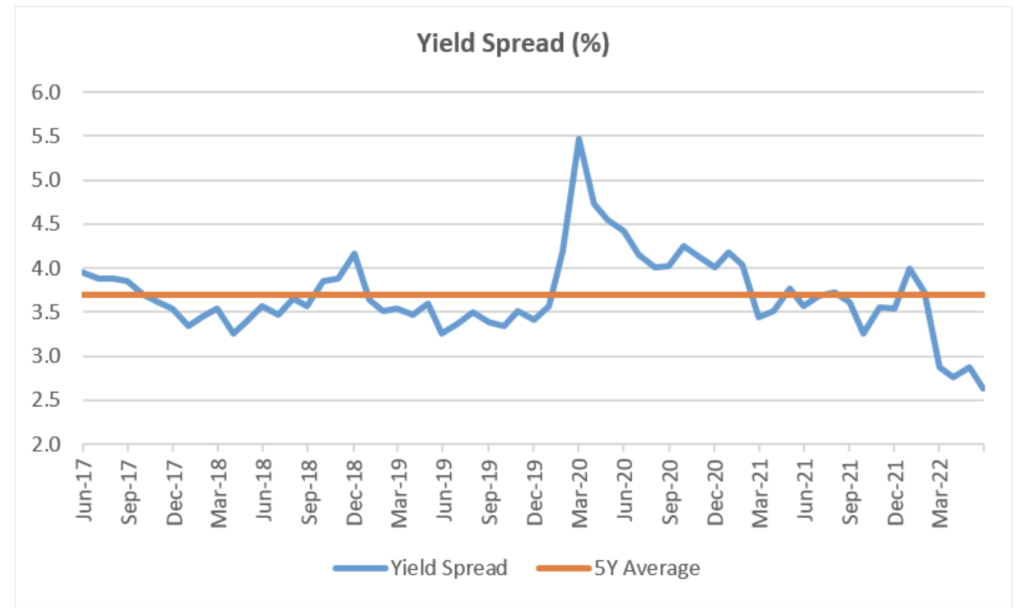

Even here in Singapore, the yield spread between the S-REIT sector and the Singapore 10-year government bond has now narrowed to 2.6% – this is significantly lower than the 5-year average of 3.7%.

For the yield spread to go back up and accurately reflect the difference in risk premiums between both instruments, then either of 2 scenarios will have to occur:

- REITs will have to pay out more dividends.

- The share prices have to decline.

If you believe that the government bond yields will go higher to 4%, and combining the historical yield spread, then investors will start expecting a yield of at least 7.5% or higher in order to adequately compensate them for the additional risk they are taking on.

This might help explain why the share price of REITs are starting to come down, and may still have more room to fall before stabilizing again.

Consider a multi-asset strategy instead

Clearly, the search for income is no longer as straightforward as before. Inflation has now soared to its highest point in decades, the global economy is grappling with supply and demand imbalances due to the pandemic and the war in Ukraine, while the Fed’s stance on monetary policy tightening is causing investors to worry about a potential recession (or even stagflation) in the coming years. What’s more, there is no precedent in history that we can take reference from – since World War 2, that has been no period where both monetary and fiscal policy have simultaneously contracted as they will be over the next 7 quarters.

We’re adapting to a new economic climate, which is why we need to monitor and actively look for higher quality investments in order to come out on top.

In the face of all these challenges, I believe that the best way forward would likely be a multi-asset strategy.

And if you are willing to broaden your search to beyond REITs and bonds, you might be surprised at the various instruments out there that can still give you decent yield, without requiring higher risk in exchange.

Strategy #1: Build a core of high dividend-paying common stocks

Build a strong core comprising of stocks that have attractive current yields, but are more importantly, in a position to increase their dividends moving forward.

To identify such companies, we can zoom into their financial statements and look out for robust free cash flows as well as a track record of growing dividends over time.

It’ll be even better if the company is in a position to pass through inflationary costs, as this will mean their profit margins will not be eroded too significantly even if cost pressures increase. An example would be real estate, which has been raising rental rates for their tenants, especially those that tend to have leases with contractual rent increases linked directly to annual inflation rates.

What’s more, the valuations of companies exhibiting such characteristics also tend to be reset higher in the face of prolonged inflation. That can then help us get higher upside returns as well.

Strategy #2: Remain nimble with fixed income opportunities

As interest rates rise, there will be more opportunity for higher yields. Short-term instruments such as high-yield bonds and floating rate notes often have higher nominal yields, a low duration and relatively lower volatility compared to equities. And unless economic growth falls dramatically, there is likely to be a low rate of defaults.

While existing bondholders are nursing substantial capital losses, the sharp selloff in bonds has now opened an opportunity to invest in various fixed income asset classes at meaningfully higher starting yields (compared to recent history).

Remaining short on duration would be prudent in this current climate, which will give you room to restructure your portfolio with higher-yield instruments should interest rates go up.

However, careful credit selection matters. Fed tightening typically leads to an increase in corporate financing costs, which may have a greater impact on the free cashflow of high-yield companies that tend to be more leveraged than their investment-grade peers. Hence, reviewing and understanding individual company default risks is important in order to maximize returns and minimize risk.

If you’re not adept in this area of due diligence, then you may wish to outsource active management of such tools to fund managers instead.

Strategy #3: Hybrid investments

Diversification of income sources will become more important as markets remain volatile.

And for investors willing to cast a wider net for income investments, there are many hybrid tools that you can use.

For instance, even among growth-style stocks that may not necessarily pay out dividends, equity-linked notes (ELNs) can help to produce income where it may not have previously existed.

What’s more, such investments offer enhanced yield, while simultaneously capturing some of the upside potential of the underlying stock.

If all this is too much for you to do on your own, you may want to consider buying a mutual fund, with a portfolio manager doing all the work for you. For example, Franklin Templeton employs the multi-asset strategy in their Franklin Income Fund, which allocates tactically to different instruments from equities to fixed income and other income-generating assets to help widen the opportunity set for potential income enhancement. You can watch how they do it here.

Using a multi-asset income strategy can help you stay the course

We know by now that time in the markets is better than timing the markets.

While many were green with envy in the last few years as growth investors showed off their outsized returns and decried value or income investing, those who then flocked to growth stocks during the peak are now sitting on massive drawdowns.

What’s worse is that many of these growth stocks typically do not pay dividends, so you’re stuck with holding the stock or selling it at a loss in order to get access to your cash.

If there’s one thing I’ve learnt over the years, it is that one’s psychological state and emotional management is key to staying invested across market ups and downs. Income investing will always have its place, and can help provide a strong sense of reassurance during volatile times like these.

Sponsored Message The Franklin Income Fund is rooted in over 70 years of history, and has delivered uninterrupted dividends through bull and bear markets since the fund’s inception in 1948. If you’re an income investor, click here to view some strategies that Franklin Templeton employs which you can consider, including the Franklin Income Fund, to help to strengthen your portfolio.

Disclaimer:

I am not your personal financial advisor and have no idea about your individual financial circumstances or actions that you need to take. You may wish to seek advice from a licensed financial adviser before making a commitment to invest in any shares of any named Funds, and consider whether it is suitable to meet your own individual goals. In the event advice is not sought from a licensed financial adviser, you should consider whether the Fund is suitable for you.

This advertisement or publication has not been reviewed by the Monetary Authority of Singapore.

This advertisement is for information only and does not constitute investment advice or a recommendation and was prepared without regard to the specific objectives, financial situation or needs of any particular person who may receive it. This advertisement may not be reproduced, distributed or published without prior written permission from Franklin Templeton. Although information has been obtained from sources that we believe to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. Any views expressed are as of the date of this post and do not constitute investment advice. The underlying assumptions and these views are subject to change based on market and other conditions. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. Franklin Templeton accepts no liability whatsoever for any direct or indirect consequential loss arising from the use of any information, opinion or estimate herein. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. The Franklin Income Fund is a sub-fund of Franklin Templeton Investment Funds ("FTIF"), a Luxembourg registered SICAV. Subscriptions may only be made on the basis of the most recent Prospectus and Product Highlights Sheet which is available at Templeton Asset Management Ltd or Legg Mason Asset Management Singapore Pte. Limited or authorised distributors of the Fund. Potential investors should read the details of the Prospectus and Product Highlights Sheet before deciding to subscribe for or purchase the Fund. This shall not be construed as the making of any offer or invitation to anyone in any jurisdiction in which such offer is not authorised or in which the person making such offer is not qualified to do so or to anyone to whom it is unlawful to make such an offer. In particular, the Fund is not available to U.S. Persons and Canadian residents. The Fund may utilise financial derivative instruments for hedging, efficient portfolio management and/or investment purposes. In addition, a summary of investor rights is available from https://s.frk.com/sg-investor-rights. Copyright© 2022 Franklin Templeton. All rights reserved. Please refer to Important Information on the website. This post is written in collaboration with Templeton Asset Management Ltd, Registration Number (UEN) 199205211E, and Legg Mason Asset Management Singapore Pte. Limited, Registration Number (UEN) 200007942R. Legg Mason Asset Management Singapore Pte. Limited is an indirect wholly owned subsidiary of Franklin Resources, Inc.