If you’ve no time to do your own investment research or monitor your portfolio, then this might just be the solution for you.

Always wanted to tap on the same investment expertise provided to high net worth investors?

Well, now you can.

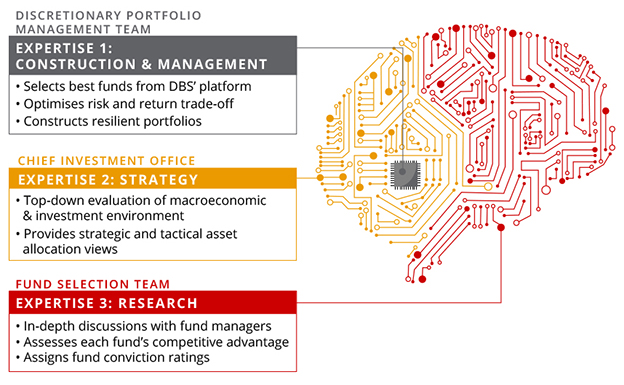

With DBS digiPortfolio, this means retail investors like you and me can finally tap on the knowledge and expertise given to the bank’s high net worth clients (those with more than S$500,000 in investment capital). The same discipline and methodology to constructing and managing a portfolio for these HNW clients is now being applied to the DBS digiPortfolio.

Their robo-investment platform uses human insights and investment strategies from the bank’s wealth management team while leveraging robo technology to automate and scale the investment offering to more investors.

The experts curate, monitor and rebalance the portfolios on your behalf. Great for those who struggle to find time to DIY their own investments, especially when the fee charged is among the lowest in the market when paying for this level of convenience.

The perks:

- Low management fee of 0.75%

- A starting sum of S$1,000 or US$1,000

- No lock-in period

- No rebalancing fees

- Saves time on research and rebalancing

There are no fees for account opening or withdrawal, and neither is there any sales charges, platform fees or switching fees that are typical of the mutual fund industry.

Instead, you pay only a 0.75% fee of your total portfolio value per year. This means that for a $10,000 portfolio, that’s $6.25 each month ($75 yearly) to cover portfolio management, investment insights, all buy/sell transactions and rebalancing.

A small price to pay for all the time and effort you get to save, and well worth getting started.

But here’s the big question on everyone’s minds:

How does it stack up against the competition?

Given the human involvement, the closest equivalent might just be mutual funds instead of the pure digital robo-advisors.

And the charges in mutual funds do not come cheap. Typically, you can expect to pay 1.5% – 2.5% total expense ratio, which covers annual management fees, rebalancing and switching fees. That’s not even including sales charges and platform fees, which works out to be another 1% – 5%.

So from this standpoint, DBS digiPortfolio is a no-brainer.

Now, if you truly believe in taking the human element out entirely, then you’ll be comparing it against the other robo-advisors here:

|

Provider

|

Rates

|

Fees per

$10,000 portfolio |

Minimum investment

|

|

DBS digiPortfolio

|

0.75%

|

$75

|

S$1,000

|

|

AutoWealth

|

0.50% + USD 18

|

$75

|

S$3,000

|

|

EndowUs

|

0.60%

|

$60

|

S$10,000

|

|

StashAway

|

0.80%

|

$80

|

None

(US$10,000) |

|

OCBC RoboInvest

|

0.88%

|

$88

|

US$2,500

|

|

UOB uTrade Robo

|

0.88%

|

$88

|

S$5,000

|

|

Smartly

|

1%

|

$100

|

S$50

|

How to Start Investing

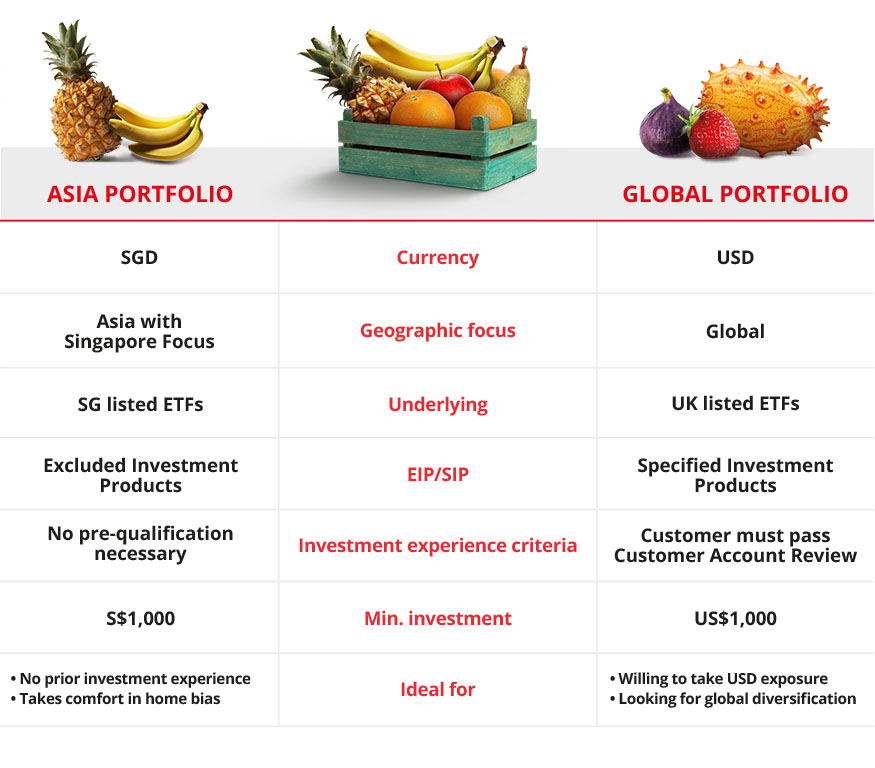

Investors can choose from between two ETF portfolios:

– Slow & Steady

– Comfy Cruisin’

– Fast & Furious

The asset mix and ETF selection in the Asia portfolio is something that no other provider in the market can offer right now, but what’s even more interesting is that DBS has chosen to go for UK-listed ETFs in their global portfolio, thus avoiding the tax problems of the US market that have plagued some of the other robo-advisors.

Which portfolio to choose will ultimately depend on your personal preference and which market you wish to gain exposure to, but personally, I’m leaning more towards the global portfolio, because there’s little to stop any Singapore investor from replicating the Asia portfolio themselves (other than the fact that the DIY approach will definitely require a larger capital than $1,000).

If you’ve never invested in the markets beyond high-yield bank savings accounts, fixed deposits, short-term endowment plans or the Singapore Savings Bonds, then the DBS digiPortfolio is a good place to start.

What’s stopping me from DIY?

Nothing.

The DBS digiPortfolio was never meant to compete against DIY investors – from a cost perspective, DIY almost always wins hands down.

You could buy the locally-listed ETFs via a low-cost brokerage and pay as little as $10 per transaction. To replicate the 4 ETFs in the Fast & Furious Asia Portfolio, that’ll cost you just $40 (although the trade-off is that you’ll need more than $1,000 for such a portfolio). Moreover, if you simply buy and hold without doing anything else. But if you were to rebalance your portfolio, you’ll have to pay another $10 each time you buy/sell any units. Depending on how many actions you make, that may or may not exceed the amount you would otherwise pay for DBS digiPortfolio.

And if you invest in the global ETFs, you’ll have to factor in recurring custodian fees and tax deductions.

We’ve not even calculated the cost of your time yet. How many hours would the market research and buy/sell transactions take you?

If you feel your time is better spent elsewhere, then this becomes a no-brainer.

As a DIY investor myself, I prefer to focus my limited time and energy to research the other portions of my portfolio that I cannot outsource, namely the stocks and property investments. When it comes to ETF investing, I’m more than happy to pay someone else to manage it for me as long as the fees are competitively low.

TDLR Conclusion

The DBS digiPortfolio is a welcome addition to the robo-advisory space, moreover when it gives us access to investment expertise that was limited to higher net worth clients only.

It also makes a lot of sense for investors who don’t have time to actively research and manage their portfolios, as well as those who have always wanted to invest but stayed out of the markets because they’ve no clue on how to construct their own well-diversified and balanced portfolio.

Even for DIY investors, for those looking to diversify and add to the index component of your portfolio, this might just be a more cost-effective and productive way to do so. It certainly saves you from all the time and extra fees incurred each time you manually rebalance your portfolio.

I definitely prefer to pay a small fee for good service, so I don’t have to worry about this portion.

And at the end of the day, investing is both a science and an art, so I’ve never once believed that technology can ever replace the human touch and judgement.

Which is why the latest launch of the DBS digiPortfolio sounds like a bank has finally gotten this part right.

This post is brought to you by DBS. All opinions are that of my own.