When I tell people about some of my recent investment wins, including several 20% – 48% gains in recent months, they tend to assume I’m talking about growth stocks in the US.

Except that I’m referring to Great Eastern (48%), DBS (25%) and Keppel DC REIT (20%), our locally listed SGX stocks. While others were flocking to shiny US stocks and artificial intelligence, I looked for strong, undervalued companies that were being neglected by the markets…and my efforts have yielded me pretty good results in a short period of time (all under 1 year).

I’ve always maintained that as an investor, we cannot afford NOT to invest in our home market. I started my investing journey in my early 20s with just Singapore stocks and bonds, and then started diversifying into the US and Chinese markets in my late 20s.

In this article, I’ll share how I’ve been building my portfolio to get capital gains and passive income from investing in Singapore.

1. Invest in fundamentally strong but undervalued companies.

A core criteria in my investing is to focus on strong, stable companies with a defensible moat and steady growth. The Singapore market has many such names, including DBS, CapitaLand, Jardine Matheson, Keppel, and more.

CapitaLand, for instance, is known as a strong property developer and asset manager not just in Singapore, but also in China, Australia and now has operations in more than 260 cities globally. Or Keppel, which operates in more than 20 countries worldwide, providing critical infrastructure and services for renewables, clean energy and more.

As these companies grow their presence in Asia, I get capital gains from holding their stock. Of course, if you don’t have time to analyse and pick individual stocks, an easy way to get exposure would be through the Nikko AM Singapore STI ETF, which gives you access to the top Singapore companies and automatically rebalances its constituents semi-annually.

2. Conduct scuttlebutt research.

Investing in Singaporean companies also gives you the chance to conduct due diligence locally to find out deeper insights and on-the-ground realities that aren’t always captured in its annual reports or on the news.

This is also known as the “scuttlebutt method”, first coined by Phil Fisher in his book “Common Stocks and Uncommon Profits” (see my list of recommended investing books here). This can involve talking to the company’s customers, employees, and doing physical, on-the-ground research to find out if the narrative being promoted by the company is indeed taking shape.

Why do customers continue to use the company’s products/services? What would motivate them to switch to a competitor? How difficult would it be for them to switch to the competition? Asking these questions help us to really assess the company’s moat and the potential switching costs involved, which makes for a more sticky business.

It was my scuttlebutt research that led me to invest in DBS above our other 2 local banks. And while all 3 have done well lately – fuelled by the rise in interest rates – DBS has outperformed its competitors by a large margin. When I travel to other Asia countries, I also see the DBS logo on buildings and bank branches more often than I do for OCBC and UOB, which reaffirms to me that DBS’ growth in Asia is faster and more widespread than its competitors.

Gains in DBS vs. OCBC vs. UOB for the last 5 years:

| DBS | OCBC | UOB |

| 48% | 28% | 15% |

Here’s another example: Grab (NASDAQ:GRAB) was just named as a top stock pick by The Motley Fool in April 2024 for its paid subscribers. But as a local here, I’m not as convinced because of what I’m seeing being practiced here.

In fact, when Grab IPO-ed back in 2020, I mentioned on my Instagram that I would not buy in because I felt it was priced at overly optimistic projections, given the on-the-ground struggles I’ve seen Grab here in Asia. Singapore is just one of Grab’s many markets in Southeast Asia, but when I travel to Malaysia, I like to ask the drivers and locals questions to see if their usage of Grab is as strong as what the narrative seems to suggest.

It is harder for me to conduct scuttlebutt research for US stocks – which is why I extended my recent US trip in Q1 this year to a grand total of 10 days so that I could at least spend some time checking out the businesses of several US stocks that I was interested in, including Shopify and Costco.

3. Dividends.

Aside from capital gains, I also invest in Singapore stocks for passive income in the form of dividends.

When I first started investing in the early 2010s, my capital was small and hence the dividends I received was puny. It was easy to dismiss a 6% yearly dividend when your portfolio capital is small, but over the years, the size of my investments grew as the underlying businesses grew and expanded.

Let’s not forget our local Real Estate Investment Trusts (REITs), which have been a mainstay for investors who seek passive income – since REITs are mandated to pay 90% of their earnings to investors as dividends (source:DBS, 2024).

Although our local REITs suffered a beating in share prices and valuations in recent years, with interest rates likely to be cut in the near term, I believe that Singapore REITs are starting to trend upwards again.

Which is why I recently invested over $50,000 into the NikkoAM-StraitsTrading Asia ex Japan REIT ETF because I felt it was oversold, and based on publicly available information on SGX, the trailing 12 month distributions – currently yielding an approximate 6% at today’s levels – were sufficient indication for me personally to get paid while I wait for the recovery in the REIT sector without having to worry about rights issues.

4. Zero taxes or forex risks.

Trending on Reddit and social media these days is the S&P 500 and its long- term attractiveness for investment. But if you’re not based in the United States, I believe that it’ll be a mistake to blindly follow this trend without knowing what you’re setting yourself up for in the future.

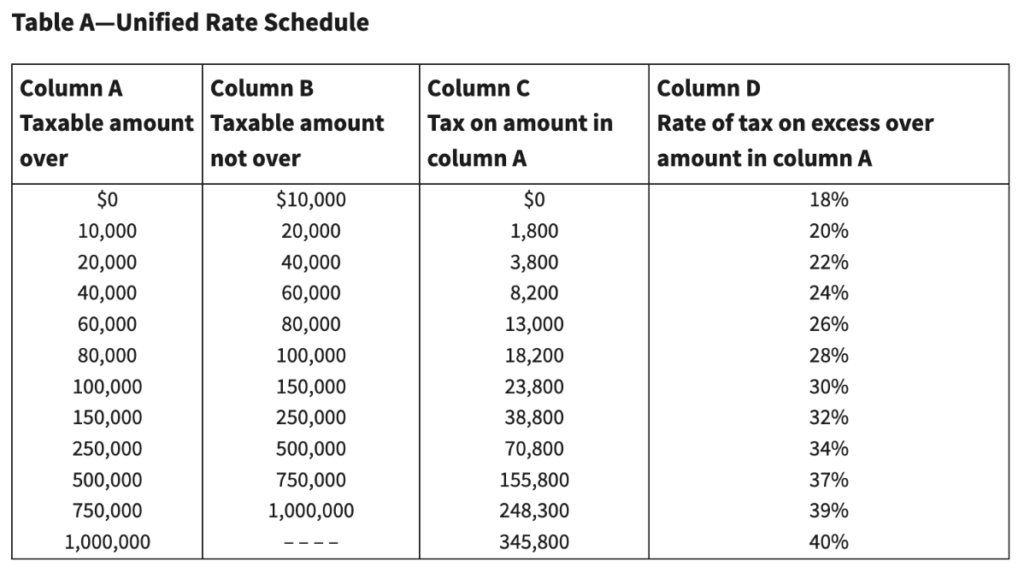

That’s because for foreign investors like you and I, the US government imposes 30% withholding taxes on dividends and up to 40% estate taxes on your US assets.

Image Source: Internal Revenue Service

But here in Singapore, we do not have to pay such taxes on our local investments. I don’t get taxed for capital gains or dividends (unlike my friends over in the US), and if anything unfortunate were to ever happen to me, my entire Singapore portfolio will go to my loved ones as an inheritance without any tax bills to be paid.

To reduce our yearly taxes, we can also make use of the Supplementary Retirement Scheme (SRS) where you can contribute up to $15,300 every year (or $35,700 if you’re a foreigner) and invest that in our local bonds, stocks or ETFs.

Other than tax concerns, another issue I had with buying beaten-down US stocks back during the March – April 2020 pandemic crash was the fact that the SGD-USD rate was at an all-time high and not in my favour.

But when we invest in Singapore, this won’t be a problem since we’ll be investing using SGD. When you’re trying to build a diversified portfolio of bonds and equities, this is also why it makes more sense for most people to do it locally without taking on any FX risk that may erode your investment returns.

Some examples are government bonds captured in the ABF Singapore Bond Index Fund, which tracks a basket of high-quality AAA-rated bonds issued primarily by the Singapore Government and quasi-Singapore government entities. Otherwise, corporate bonds issued by stable, blue-chip issuers such as NTUC Income or Temasek can be accessed through the Nikko AM SGD Investment Grade Corporate Bond ETF without having to lock up so much cash in a single, institutional bond alone.

TLDR: Don’t underestimate the potential gains you may make investing in Singapore.

In recent years, most young investors I meet at events have been telling me that they own US stocks or cryptocurrencies, but few speak of our local SGX investments.

I can understand why. The majority of financial influencers on social media talk about these things, especially given how well the US markets have done in the last year.

If you look over at Reddit, the same narrative is being propagated – invest in the S&P 500 using dollar-cost averaging and ignore everything else. As such, new investors may believe that investing in the US is the only way to go.

But this is a form of recency bias, where investors expect similar returns from the past to repeat in the future. And in my opinion, the most popular (or most echoed) way…may not always be the best way. Especially if you’re trying to beat the market.

As an investor, you want to look where others are not looking.

I’ve used this approach for years and it has worked fantastically well for me.

This is why my exposure to Singapore stocks and bonds continue to form a core foundation in my investment portfolio. While many younger investors are flocking to US stocks and cryptocurrencies for quick capital gains, I maintain a balanced approach in the way I invest – which includes being vested in my home country (Singapore) for undervalued stocks and passive income through dividends. And what better time than now with Singapore’s 59th birthday coming up! Majulah Singapura!

Disclosure: This post is brought to you in collaboration with Nikko Asset Management Asia Limited (“Nikko AM Asia”). All research and opinions are that of my own. Investments involve risks, including the possible loss of principal amount invested. None of the stocks or ETFs mentioned here are a BUY or SELL recommendation; you should use this article as a starting point to get ideas for your own investment portfolio and make your own decisions instead. And if you wish to learn more about the various ETFs offered by Nikko AM Asia which you can use for SRS and CPF investing, click into the respective links above to retrieve the fund prospectus and performance so as to help you decide whether it fits into your investment objectives.

Important Information by Nikko Asset Management Asia Limited:

This document is purely for informational purposes only with no consideration given to the specific investment objective, financial situation and particular needs of any specific person. It should not be relied upon as financial advice. Any securities mentioned herein are for illustration purposes only and should not be construed as a recommendation for investment. You should seek advice from a financial adviser before making any investment. In the event that you choose not to do so, you should consider whether the investment selected is suitable for you. Investments in funds are not deposits in, obligations of, or guaranteed or insured by Nikko Asset Management Asia Limited (“Nikko AM Asia”).

Past performance or any prediction, projection or forecast is not indicative of future performance. The Fund or any underlying fund may use or invest in financial derivative instruments. The value of units and income from them may fall or rise. Investments in the Fund are subject to investment risks, including the possible loss of principal amount invested. You should read the relevant prospectus (including the risk warnings) and product highlights sheet of the Fund, which are available and may be obtained from appointed distributors of Nikko AM Asia or our website (www.nikkoam.com.sg) before deciding whether to invest in the Fund.

Distributions are not guaranteed and are at the absolute discretion of Nikko AM Asia. Past payout yields and payments do not represent future payout yields and payments. If the investment income is insufficient to fund a distribution for the Fund, Nikko AM Asia may determine that such distributions should be paid from the capital of the Fund. Any distribution is expected to result in an immediate reduction of the Fund’s net asset value per unit.

The information contained herein may not be copied, reproduced or redistributed without the express consent of Nikko AM Asia. While reasonable care has been taken to ensure the accuracy of the information as at the date of publication, Nikko AM Asia does not give any warranty or representation, either express or implied, and expressly disclaims liability for any errors or omissions. Information may be subject to change without notice. Nikko AM Asia accepts no liability for any loss, indirect or consequential damages, arising from any use of or reliance on this document.

This advertisement has not been reviewed by the Monetary Authority of Singapore.

The performance of the ETF’s price on the Singapore Exchange Securities Trading Limited (“SGX-ST”) may be different from the net asset value per unit of the ETF. The ETF may also be suspended or delisted from the SGX-ST. Listing of the units does not guarantee a liquid market for the units. Investors should note that the ETF differs from a typical unit trust and units may only be created or redeemed directly by a participating dealer in large creation or redemption units.

The Central Provident Fund (“CPF”) Ordinary Account (“OA”) interest rate is the legislated minimum 2.5% per annum, or the 3-month average of major local banks' interest rates, whichever is higher, reviewed quarterly. The interest rate for Special Account (“SA”) is currently 4% per annum or the 12-month average yield of 10-year Singapore Government Securities plus 1%, whichever is higher, reviewed quarterly. Only monies in excess of $20,000 in OA and $40,000 in SA can be invested under the CPF Investment Scheme (“CPFIS”). Please refer to the website of the CPF Board for further information. Investors should note that the applicable interest rates for the CPF accounts and the terms of CPFIS may be varied by the CPF Board from time to time.

Neither Markit, its Affiliates or any third party data provider makes any warranty, express or implied, as to the accuracy, completeness or timeliness of the data contained herewith nor as to the results to be obtained by recipients of the data. Neither Markit, its Affiliates nor any data provider shall in any way be liable to any recipient of the data for any inaccuracies, errors or omissions in the Markit data, regardless of cause, or for any damages (whether direct or indirect) resulting therefrom. Markit has no obligation to update, modify or amend the data or to otherwise notify a recipient thereof in the event that any matter stated herein changes or subsequently becomes inaccurate. Without limiting the foregoing, Markit, its Affiliates, or any third party data provider shall have no liability whatsoever to you, whether in contract (including under an indemnity), in tort (including negligence), under a warranty, under statute or otherwise, in respect of any loss or damage suffered by you as a result of or in connection with any opinions, recommendations, forecasts, judgments, or any other conclusions, or any course of action determined, by you or any third party, whether or not based on the content, information or materials contained herein. Copyright © 2023, Markit Indices Limited.

The Markit iBoxx SGD Non-Sovereigns Large Cap Investment Grade Index are marks of Markit Indices Lmited and have been licensed for use by Nikko Asset Management Asia Limited. The Markit iBoxx SGD Non-Sovereigns Large Cap Investment Grade Index referenced herein is the property of Markit Indices Limited and is used under license. The Nikko AM SGD Investment Grade Corporate Bond ETF is not sponsored, endorsed, or promoted by Markit Indices Limited.

The units of Nikko AM Singapore STI ETF are not in any way sponsored, endorsed, sold or promoted by FTSE International Limited ("FTSE"), the London Stock Exchange Plc (the "Exchange"), The Financial Times Limited ("FT") SPH Data Services Pte Ltd ("SPH") or Singapore Press Holdings Ltd ("SGP") (collectively, the "Licensor Parties") and none of the Licensor Parties make any warranty or representation whatsoever, expressly or impliedly, either as to the results to be obtained from the use of the Straits Times Index ("Index") and/or the ¬figure at which the said Index stands at any particular time on any particular day or otherwise. The Index is compiled and calculated by FTSE. None of the Licensor Parties shall be under any obligation to advise any person of any error therein. "FTSE®", "FT-SE®" are trade marks of the Exchange and the FT and are used by FTSE under license. "STI" and "Straits Times Index" are trade marks of SPH and are used by FTSE under licence. All intellectual property rights in the ST index vest in SPH and SGP.

The NikkoAM-StraitsTrading Asia ex Japan REIT ETF (the “Fund”) has been developed solely by Nikko Asset Management Asia Limited. The Fund is not in any way connected to or sponsored, endorsed, sold or promoted by the London Stock Exchange Group plc and its group undertakings, including FTSE International Limited (collectively, the “LSE Group”), European Public Real Estate Association ("EPRA”), or the National Association of Real Estate Investments Trusts (“Nareit”) (and together the “Licensor Parties”). FTSE Russell is a trading name of certain of the LSE Group companies. All rights in FTSE EPRA Nareit Asia ex Japan REITs 10% Capped Index (the “Index”) vest in the Licensor Parties. “FTSE®” and “FTSE Russell®” are a trade mark(s) of the relevant LSE Group company and are used by any other LSE Group company under license. “Nareit®” is a trade mark of Nareit, "EPRA®" is a trade mark of EPRA and all are used by the LSE Group under license. The Index is calculated by or on behalf of FTSE International Limited or its affiliate, agent or partner. The Licensor Parties do not accept any liability whatsoever to any person arising out of (a) the use of, reliance on or any error in the Index or (b) investment in or operation of the Fund. The Licensor Parties makes no claim, prediction, warranty or representation either as to the results to be obtained from the Fund or the suitability of the Index for the purpose to which it is being put by Nikko Asset Management Limited.

Nikko Asset Management Asia Limited. Registration Number 198202562H.

All information in this article is accurate as of 8 August 2024.