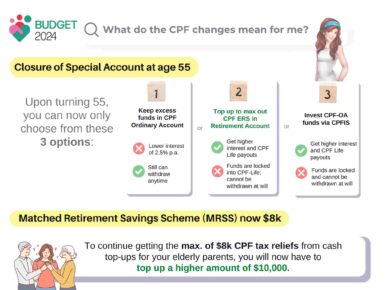

The issue of CPF was a popular one during elections season raised by many of the opposition parties, especially given how thorny the issue is.

Indeed, the CPF system is a painful one. As a fresh graduate earning on $2,500 not too long ago, it was depressing to only get slightly more than $1,800 each month for living expenses. (If you’re thinking that should be $2,000 instead, you’re right – I actually suspect now that the accounts were incorrect, but back then I wasn’t financially savvy enough to flag out my employer for it. Oh well.)

So what were the different opposition parties saying about the CPF? I won’t go into detail here, but if you’re interested, here’s a really skeptical breakdown provided by MoneySmart that I like.

With the exception of the Workers’ Party, I personally think that the rest of the opposition parties got it wrong.

AK has got some really good pieces on CPF but there’s one main article highlighting the facts that I think every Singaporean should know. I’ve combined his words (in blue) with some additional points of my own below. (Thanks AK!)

As written by Kelvin Tan (The Edge, June 2014):

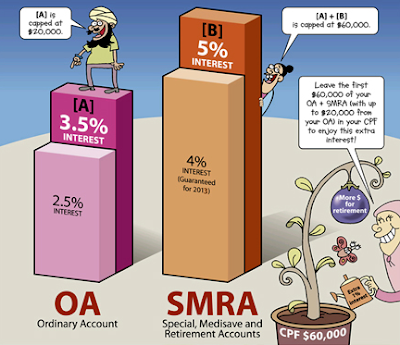

1. It is not easy beating the Ordinary Account’s guaranteed interest rate of 2.5%

“It may sound easy, but beating the OA’s guaranteed annual interest rate of 2.5% is by no means an effortless task for CPF members who are looking to grow their savings under the CPFIS (CPF Investment Scheme).

Indeed, only 15% of CPF members who sold their CPFIS-OA investments for FY2013 ended September 30 made profits in excess of the OA interest rate of 2.5%.

42% of these CPFIS-OA investors actually incurred losses in FY2013″.

2. Your Special Account funds are already earning decent returns of 4% – 5% annually.

“While it makes sense for savvy long-term investors to invest their excess OA money, some financial advisors advise their clients not to take any risks with their SA money which is already earning decent returns of 4% to 5% a year.”

3. What can you do to maximize your CPF earnings?

If you’re generally risk averse, you can consider transferring the funds in your OA to SA, where you can earn higher interest rates.

Many financially savvy folks who know how to take advantage of the CPF system for their own benefit are already contributing cash to top up their SA to the Minimum Sum, which also allows them to enjoy tax reliefs of up to $7,000 per calendar year.

“Singaporeans should look at their CPF SA like the bond portion of their overall portfolio… In their retiring years, they should look at their CPF Life as their annuity investment, giving them a monthly amount for life.

Singaporeans who generally have little in their CPF accounts should start saving more, do early retirement planning and invest prudently with a long-term view to growing their nest eggs rather than demand higher interest rates on their CPF savings.”

“As for Singaporeans who have highlighted that other countries such as Malaysia and India pay higher interests in similar pension schemes, my view is that they forget our Singapore dollar is rated AAA and has appreciated against the currencies of many other countries”, said William Cai, a GYC financial advisor.

4. Budget Babe’s recommendations on CPF

Why do a lot of people favour the opposition’s calls for #ReturnOurCPF, especially for a lump sum withdrawal at age 55?

My guess is grounded in basic human psychology – given a choice between immediate benefits and delayed gratification, most people tend to choose the former.

But if you’re willing to deal with the short-term pain, you are going to be heavily rewarded later on.

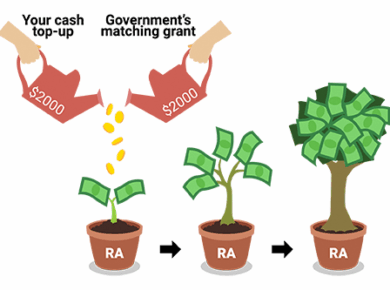

Step 1: Earn more money from the government by maximizing your SA.

Contributing $500 in cash every month is a good start.

The interest rates for our SA is the highest among all our CPF accounts. If we start channeling more money into our SA early enough, we will soon see the magic of compounding setting in.

How many investments give you a guaranteed interest rate of 4% – 5%, RISK-FREE?

|

| Photo credits: www.gov.sg |

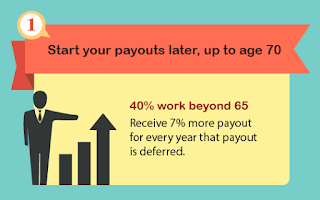

Step 2: Make the government give you more money by delaying your payouts

|

| Photo credits: www.gov.sg |

Step 3: Secure your post-retirement payouts by making sure you do NOT buy a house beyond your means.

It is very tempting to buy a 5-room HDB, but can you afford it?

Many young Singaporeans get a 5-room flat for their first purchase without realizing that they’re losing out on almost $40,000 worth of grants. Even if you downgrade later, you would have already unknowingly chosen to forgo your eligibility for further grants.

If you and your spouse earn less than $5,000 combined a month, you might want to consider buying a 3-room HDB flat for a start first. Aside from all the grants available to help you offset your purchase, you can also always upgrade later on if you like.

With love,

Budget Babe

10 comments

Good post BB. I quite like how AK frames CPF to be the "bond" portion of your portfolio. The interest rates quite easily beat most "investment insurance / endowment" products, especially if it qualifies for the bonus 1% interest.

Perhaps I am a bit more aggressive, but I would consider "breaking the piggybank" and make use of the CPFIS schemes in a big bear market. That is if I have enough money over the minimum limits to use those schemes, haha!

I used to do cash top up to SA as well until i realise that these top ups will be locked into the CPF life even if you meet the full or basic retirement sums. I am uncomfortable with that since the payout eligibility age is not within our control. I have stopped doing so since. But i would consider transfering OA to SA.

A cash top up to SA and subsequently being able to withdraw it will only work if you are able to meet the min sums. Meeting the minimum sums is fairly easy for if one continuously works from age 25 to 55 and earns the average pay of your cohort.

I agree that one should view CPF as a "bond" portfoilo and it is indeed true that the CPF SA easily beats most investment insurance/whole life etc

After we have paid up our housing loan, I persuaded my wife to transfer the balance in her OA to SA till it hit the min sum. When she reached 55, after setting aside the min sum, she still has a few hundred thousands in her CPF account!.

I don't have as much as I used my OA money to top up my parents' retirement accounts, but my parents benefitted from it.

I thought so too initially, until I probed CPF board. Here's what CPF board said to me in an email:

"The top-up monies in the recipient’s Special Account and the interest earned will be transferred to his Retirement Account when he turns 55 and it cannot be withdrawn even with a property pledge."

Hi GMGH!

Indeed, in a strong bear market the CPFIS scheme can actually help us to make good money, provided we know how to put them into the right investment products. However, for most Singaporeans who don't know much about finance and investing, redeeming the 4% – 5% compounded interest on their SA is already extremely rewarding especially if they start early.

Hi Betta Man,

Those are valid reasons. I'm not too worried about the payout age though, since the later it is, the more money I'm earning from the government in the form of interest anyway, so I'm okay with putting more into my SA until it reaches MS 🙂

Hi Choon Yuan,

You're right. Like you said, if we start early, it is not difficult to meet the MS at all. Even if we start in our 30s, if we contribute cash, it is still not too late to meet the MS and allow the magic of compounded (high) interest rates set in 🙂

Hi Betta Man,

I guess it depends on how you view the CPF. If you look at it as solely a retirement nest egg (which is what it is designed to be), then that does not matter too much. But if you're looking at it as a form of investment where you can take out your money to spend, then yes, the problems with not being able to withdraw everything can be uncomfortable to some.

Your wife is lucky to have your wise advice 🙂 hundreds of thousands – I believe that was after the effect of compound interest as well?

Congrats!

Comments are closed.