The drama surrounding Eagle Hospitality Trust (SGX:LIW) continues to intensify.

Shareholders of EHT have been stuck for months now because they cannot sell the stock (due to the trading suspension) and they are not going to receive any dividends. For anyone who relies heavily on REITs and/or Business Trust to fund your passive income / retirement cashflow, let this be a warning tale of a REIT investment gone wrong. *While there are inherent differences between a REIT and a Business Trust, I’ll use the terms interchangeably in this article for simplicity reasons.

(Or will there be a turning point? That will depend on whether EHT and its Sponsor, can work together to save the failing business.)

I designed this image below to sum up my thoughts on this entire saga:

Background:

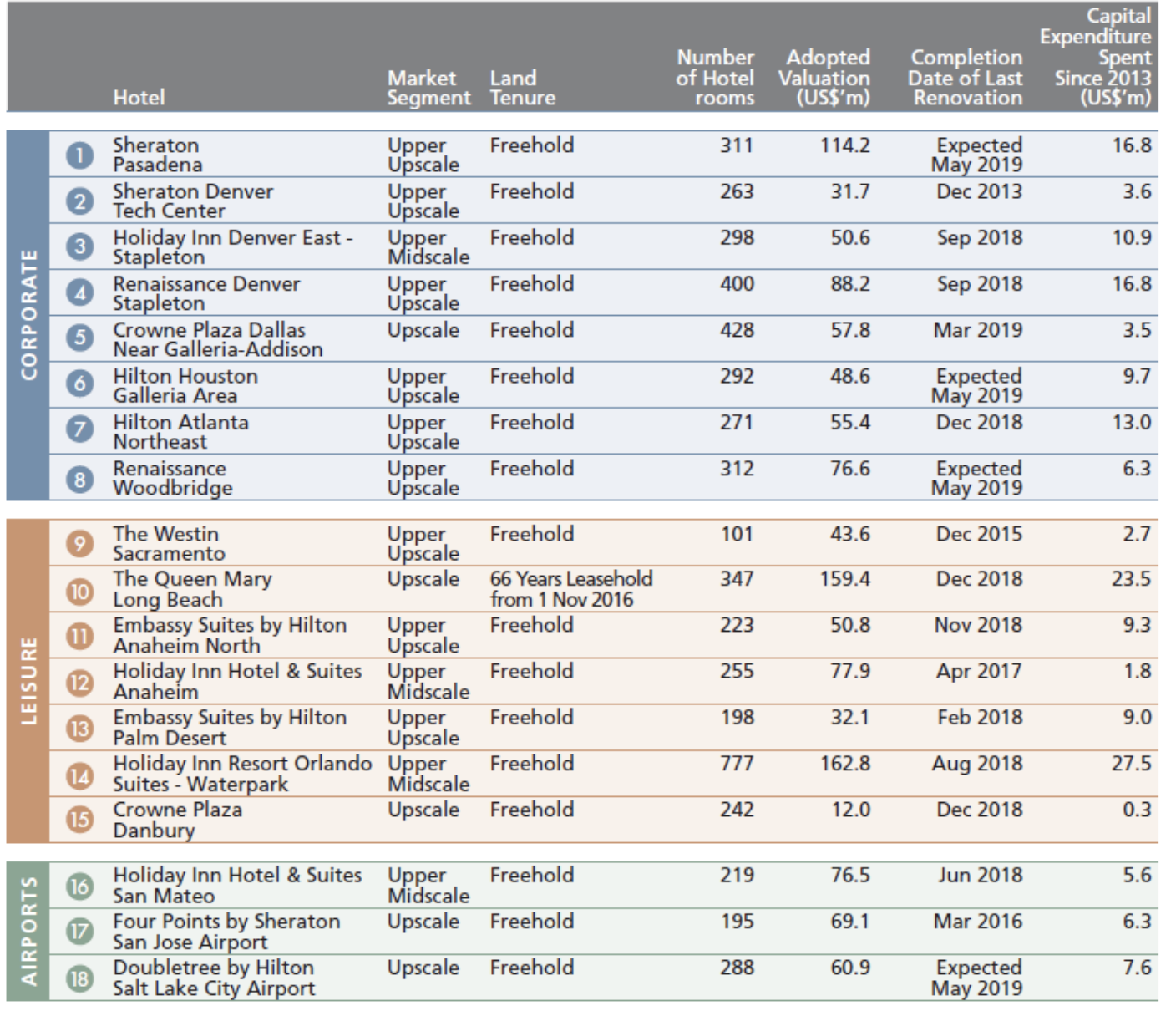

When EHT first IPO-ed in Singapore last year, it looked like a promising investment with its portfolio of 17 freehold hotels and 1 leasehold ship located across the US, worth US$1.27 billion in total. Some of its hotels included the Sheraton, Hilton, the Westin, Crowne Plaza…while the leasehold ship was the Queen Mary, permanently docked at California.

With a projected yield of 8.1% in 2020, it seemed like a promising thesis play on the growing US hospitality sector. Its Sponsor was Urban Commons LLC, whose portfolio included 14 hospitality assets, of which 12 were injected into Eagle for the IPO listing.

Compared to other hospitality trusts, EHT had a higher gearing level, but in turn offered the highest yield and the second-lowest Price-to-Book ratio. If you prefer to reference a more comparable peer, that would then be ARA US Hospitality Trust (the other pure-play US hospitality REIT listed in Singapore), which had full exposure to variable rents. EHT thus seemed like a safer choice for risk-adverse shareholders given its 66% fixed rental income component.

Investment Opportunity?

Some investors went in at IPO, whereas others chose to wait for a better price opportunity after seeing how ARA’s listing saw its share price go down after IPO. In November 2019, an opportunity arrived when EHT’s share price plummeted after bad news of the Queen Mary ship falling into disrepairs came to light. Many financial bloggers – including yours truly – saw this as a potential turnaround play, since the Queen Mary made up only 1/18 of EHT’s total asset portfolio. I documented my investment thesis and calculations then in this post.

Alas, more bad news continued coming and shortly after, EHT shares were suspended on SGX and we ended up being stuck with a stock counter that we could neither sell, nor buy more of. Well, at least there’ll still be dividends…?

As luck would have it, Covid-19 then struck and we all know how the rest of the story goes. The hospitality industry takes a huge hit due to the travel bans, and the price of hospitality REITS (and other stocks) fall worldwide. As the economic recession prolongs, experts are now worrying about the impending rental defaults that they expect to happen very soon.

Now, as a shareholder stuck with EHT stock (or any other hospitality-related stock, really) during this time, I’d normally just hold on and ride the wave out. Based on my usual strategy and if the balance sheet of the company looks like it has enough cash to ride out the prolonged crisis, I may even make more opportunistic purchases and average down at lower stock prices.

However, I can’t do that with EHT. And even if I could, I am not sure if I would, because the problems of EHT seems to run deeper.

What worries me the most about EHT is:

The drama and ongoing spat between EHT and its Sponsor, Urban Commons.

This is where you need to start paying attention, especially if you’re invested in EHT as well.

In recent SGX filings (and various reports by the Business Times), we’ve been served with bad news after bad news from the perspective of EHT. However, in recent emails that EHT’s communications team has sent to me, it suggests that the public has not been told the full story.

The fight seems to be between EHT and its Sponsor, and boy, the plot seems to be thickening!

Confused? While there’s several moving parts to the saga, here’s some key issues that caught my attention, and which I feel all shareholders should question as well.

Eagle Hospitality Trust accused its Sponsor Urban Commons of making unauthorised loan applications on its behalf and not sharing the loan proceeds with them

TLDR Version:

- EHT flags out unauthorised loan made by Urban Commons on its behalf and asks why the loan proceeds were not shared with them.

- Urban Commons says it was a mistake and they are already transferring the funds to the rightful applicant, the US tenant.

- Urban Commons accuses EHT of “using a SGX announcement to draw public attention and outrage without putting the matter in its proper context”.

I’ve summarized the story below:

In a SGX filing on 14 August 2020, EHT claims that it discovered an unauthorised loan application was filed by its Sponsor, under the US Paycheck Protection Program – similar to Singapore’s Job Support Scheme – on its behalf. It goes on to say that no portion of the US$2 million loan proceeds was received or shared with the Queen Mary master lessor (landlord) i.e. EHT.

Its Sponsor, Urban Commons, has responded by saying it made a mistake in submitting the loan application – the landlord of the Queen Mary is foreign owned (EHT is considered to have non-US ownership), meaning EHT is in fact not eligible for a loan under the US government’s paycheck protection program.

While EHT maintains that the loan was approved and US$2 million was provided, Urban Commons states that they rectified the mistake with the US government and has already provided all the necessary documentation to transfer the loan to the tenant. But despite having done this, and informing EHT together with its advisors, Urban Commons argues that EHT is “targeting [Urban Commons] with misconceived allegations, further damaging [Urban Commons] reputation without cause”.

Q3 FY2019: Hurricane damage strikes its largest hotel

And, as (bad) luck would have it, Covid-19 was not the only Force Majeure event that happened. EHT’s largest portfolio asset – the Holiday Inn Resort Orlando Suites – had its business affected by another Force Majeure event which was, in this case, a Category 5 Hurricane Dorian. Many guests scrambled to cancel their room reservations, and occupancy rates plummeted to 27%, thus affecting EHT’s Q3’s DPU.

EHT and shareholders have questioned about why this was not claimable under insurance, and Urban Commons said that it did not qualify for it (based on the minimum policy deductible), despite having incurred business losses and property damage.

With the above two adverse events, EHT thus decides to withhold payouts, despairing many retail investors who were waiting to be paid their dividends.

Q2 FY2020: Eagle Hospitality Trust reports a sizeable loss and attributes it to loss of rental

They posted a loss of USD38.9 million for the period, stating that this largely stemmed from from impairment loss on trade receivables amid uncertainty from master lessees’ ability to make rental payments.

Note that rental is payable by Urban Commons to EHT, so you can see what EHT is driving at…

That sounds completely reasonable…until you start to think about how the Covid-19 pandemic was an unprecedented event and wonder, could the rental contracts have had a Force Majeure clause?

As Urban Commons points out, there is. And due to any Force Majeure event, the Sponsor (Urban Commons) and its tenants (includes Urban Commons, together with some others) are not liable to guarantee continued operation of EHT’s properties or pay rental.

Urban Commons issues a breach notice to EHT on monies owed

Here’s where the drama intensifies.

About a week ago, Urban Commons issues a notice of breaches to EHT, stating that funds it had injected into EHT are outstanding and due for repayment.

Hang on, didn’t EHT just say its tenants (Urban Commons) owed it rental? How come now Urban Commons is saying EHT owes it money?

If you’re confused, you’re not the only one. But that apparently seems to be the case – Urban Commons says it does not owe EHT rental due to the Force Majeure conditions, and that EHT owes them money instead for the funds that Urban Commons injected into EHT as a Sponsor.

Urban Commons says it has a plan; accuses EHT of non-cooperation and wasting unnecessary funds

In its latest press releases (and upon the urging of their communications team for me to run this story so that minority shareholders are kept “informed”), Urban Commons says it has repeatedly communicated a plan to EHT’s trustee to provide critically-needed financial support, but has not received cooperation from EHT’s side to implement and save the REIT.

- Refinance the defaulted debt quickly with a term sheet (which UC says they already have it prepared and ready to execute)

- Raise capital to sustain the REIT and minimize further dilution to shareholders

- Come up with an amicable solution to restart and sustain the operations of the REIT

So who’s the bad guy here? EHT or Urban Commons?

As you can see, there are a lot of strong accusatory statements made (by both parties), and I truly hope that SGX RegCo investigates this.

EHT’s troubles now may very well be just temporary, but if the fight between EHT and Urban Commons continues, then I wouldn’t be surprised if the business sinks to the point of no return.

Urban Commons claims that as its Sponsor, it already has a plan to save the REIT.

So why is EHT being uncooperative?

Why is EHT not working with its Sponsor to refinance and save the business?

Why do both parties have to continue firing accusations against one another, and sour the relationship further?

I appeal to SGX RegCo to intervene at this point and make both parties work together.

As a shareholder, we should be asking EHT if there’s any validity to Urban Commons’ claims, and why this is happening. If EHT insists that Urban Commons is in the wrong here, then let us watch and see how their plan fails. Because at this moment in time, EHT has yet to give a satisfactory answer to retail shareholders on how it intends to turn things around…all we see is bad news after bad news and a blaming game.

We, your minority shareholders, deserve answers.

Disclaimer: This story and my opinions of the ongoing saga were written based on SGX filings (by EHT), several press releases and posts by Urban Commons. All statements of facts and claims are based on the statements of the original parties, and are not mine. Budget Babe makes no accusation towards either party and simply wants everyone to work together to save the business trust. Thank you.

1 comment

Investment plansPROMO PACKAGE �� BASIC Invest $70 earn $600 Invest $100 earn $1000 Invest $200 earn $2,000 Invest $300 earn $3,500 Invest $400 earn $4,500 Invest $500 earn $6,000

�� PRO Invest $1,000 earn $15,000 Invest $2,000 earn $25,000 Invest $3,000 earn $35,000 Invest $4,000 earn $45,000 Invest $5,000 earn $60,000 Invest $10,000 earn $100,000.

�� PREMIUM 1BTC earn 5BTC 2BTC earn 10BTC 3BTC earn 16BTC 4BTC earn 22BTC 5BTC earn 30BTC.

ALL RETURNS ARE SCHEDULE, FOR 12 HOURS, UPON CONFIRMATION OF PAYMENTS.

MODE OF PAYMENT. Any, Suitable For Investors, But Terms and Conditions Apply.

⭐️HURRY NOW!!! Refer a Friend or Family member to invest same time, and Receive an instant $50 Reward.

To set up an INVESTMENT PLAN, Contact Admin: totalinvestmentcompany@gmail.com

WhatsApp: +1(929)390-8581

https://www.facebook.com/pg/Total-Investment-221964325813140/about/

https://t.me/totalinvestment

Comments are closed.