Ever since Aspial Corporation Limited launched their 5.25% retail bonds (i.e. you get 5.25% returns on your money) a few days ago, I’ve received a number of messages from readers and friends asking if they should sign up for these bonds.

Before we delve into the research, we must first understand what bonds are for and how they work.

Bonds are a type of investment that offer a fixed interest rate and guaranteed capital return upon their maturity. They’re a crowd favourite with many investors given their risk-free nature and interest rates that are higher than keeping your money in the bank. Furthermore, the guaranteed nature of bonds makes them a resilient investment tool regardless of the economic situation. During recessions, bonds are often the only tool that continue to maintain their interest rates.

But why risk-free? Note that while not all bonds are free from risks, most of them generally are. In Singapore, most of our bonds are issued by the government. What are the odds of the Singapore government going bust? It is also an open secret that Singapore has one of the most generous reserves in the world. How much exactly, we don’t really know, but 50 years of history has shown that our trusty government has never failed to bail us out of any crisis before.

Note: This is also a common sales tactic used by insurance agents in asking you to buy ILPs. They are not wrong, but you should never take anything they say at face value.

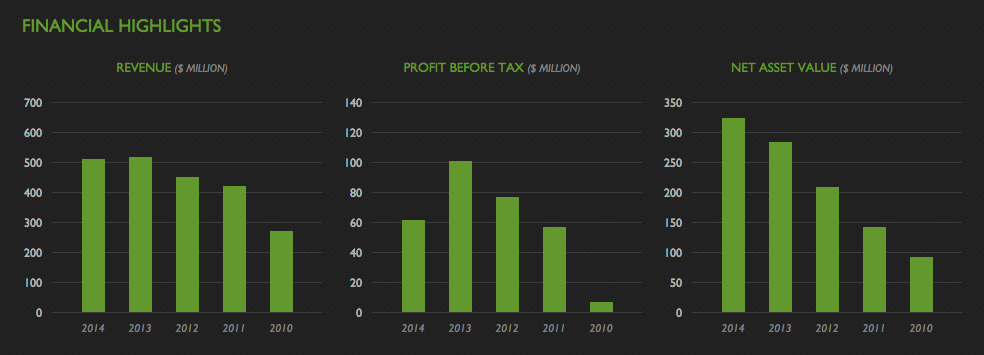

Looking at their Investor Relations page, their numbers seem pretty good (read from right to left). Their net asset value (NAV) and revenue has been increasing, and so have their profits – except for last year.

Given their profile and with their bonds offer at a 5.25% interest rate, Aspial bonds do appear to be immensely attractive. All you need to do is invest a minimum of $2,000 and wait out for 5 years, while you eat, sleep and collect returns without doing anything else.

Of course, there’s no such thing as a free lunch in this world. What’s happening here? This is where we need to ask some important questions.

1. Why are Aspial raising these bonds?

According to Aspial, it hopes to raise over $70 million to “refinance borrowings, increase working capital and fund future business investments”.

This sounds fine, but again, you shouldn’t take what the company says at face value. So I went to check out their debts, which was relatively stable, hovering around 70% of their total assets each year. Pretty healthy.

2. Why such a high interest rate?

As the age-old adage goes, high risks…high returns.

I wondered if Aspial is offering such a high interest rate in order to attract more people to buy into their bonds and thus provide them with the funding that they need. Sometimes, companies with bad credit or financial health may get rejected by the banks for loans, and therefore need to turn elsewhere to raise funds. Could this be the case here?

We can only look at their numbers to find out.

3. Can they pay off their debts?

This was where I found the first warning signal.

Their cashflow has been negative for the past 5 years from their operating and investing activities. Although net change in cash is still positive, it seems to be driven by the high financing (debts) that they’re taking on.

|

| Credits: SGX |

Investors who only looked at the current ratio would not have picked this up as the current ratio is still quite acceptable.

With a possible impending economic slowdown, commodity prices like gold may shoot up as more people turn to these stable instruments to buffer against the decline.

Furthermore, if the economic depression really hits us, more people may lose their jobs, leading to them becoming desperate and possibly end up having to pawn their valuables for cash in order to survive. Should this happen, the supply is likely to then exceed the demand, which could result in MaxiCash benefitting from getting valuables at depressed prices.

Otherwise, should interest rates rise, Aspial will then have to repay even higher interest on their loans.

5. What are the odds of Aspial defaulting?

One might be tempted to conclude that the odds of Aspial folding up and closing the business entirely is not very possible. After all, they own some of the largest jewellery brands and so many retail stores all over Singapore.

However, there is ALWAYS a risk that a company might go bust, no matter how small the risk may be. Between the government (SGS bonds) and Aspial, who do you think is more likely to collapse, if any at all?

6. What other red flags are there?

(i) Showing selective financials on the main page

The first thing that made me sit up in shock was when I realized how their Investor Relations team showcased financial data on their main page which puts Aspial in a good light.

Remember that first graph above on Aspial’s rising revenue?

Well, if you examine closer, you’ll realize that while revenue has technically increased, their net income has in fact been decreasing.

What happened?!

This is what good PR folks do 😉 thankfully, I’m a PR consultant myself, so I can spot some of these tactics faster than most people.

(ii) Too much publicity about the bonds

Considering how many announcements and advertisements they have put out to publicize the bonds, it reeks of desperation to me. How badly do they need to raise the money?

(iii) Lovely marketing terms

I do support local companies, but if the company isn’t a good one, I personally rather not own it.

I teach my GP students how to analyze arguments in depth, and most of my students will be able to tell you that this sentence is a way to make you feel good, as it sends the implied message that if you’re sophisticated, you’ll definitely choose to invest in them.

While my analysis suggests that Aspial’s bonds may not be as attractive as they sound, no one knows for sure what will happen in the future. If Aspial is able to use these funds to bail themselves out of the crisis over the next few years, they might be able to bounce back stronger than before.

But if Aspial can’t ride out the crisis, there’s a very real possibility that they may default on their loans which means we retail investors won’t even get our capital back.

Thus, given the risks, if I’m afraid to lose my money, the upcoming Singapore Savings Bonds (SGS) is a better choice, as the risk of the Singapore government defaulting is much lower compared to Aspial.

However, if I have some spare cash that I do not need, I might buy a small portion of their bonds. But if I were to put about $3,000 with them, I will prepare myself mentally to be prepared to kiss this money goodbye forever.

Or, if I have lots of money / have plenty of confidence that Aspial will ride out this crisis, I will put a huge chunk of my money with them and simply wait for the 5 years to be up. After all, 5.25% on $100,000 is worth more than the median monthly salary here, and I don’t even have to do anything! No research or financial calculations. Nothing.

If you wish to apply, you have 3 more days.

So what do you plan to do? Or have you already applied for their bonds? Do share with me below!

Update (April 2016): Guess what? It has hardly been a year but Aspial launched another round of bonds offering 5.3% yield with a $200 million tranche for retail investors again, despite already being highly-leveraged. I mentioned during their previous round that if I were to park my money with them, I’d be prepared to kiss the sum goodbye, so it isn’t surprising that they’ve pulled off another round of fund-raising again. What IS surprising, though, is how oversubscribed this round’s tranche was (almost 5x)!

With love,

Budget Babe

3 comments

Some other factors that might be useful from an analytical standpoint would be to think through the sources for repayment, security assigned to this debt and priority ranking in the capital structure.

* Sources of repayment – Have a think about what would be the most likely form of repayment. Would it be cash flows from operations? Divestment of assets? Or through refinancing / equity raising?

* What security is afforded to this Facility? This seems like an unsecured facility, meaning that in the event of default, it can only enjoy repayment from proceeds of liquidated unsecured net assets, on a pari passu (equal ranking) basis with all creditors

* Capital and corporate structure is important. Is this facility sitting at the holding company level (shell with minimal assets) or does it sit at an operating company level? How many creditors rank ahead of this? This affects repayment in a liquidation scenario, in tandem with security.

Holdco debt tends to have higher pricing but are unsecured. Have not read the OC on this and am not sure what Aspial really does (contribution from individual operating segments), but I would think for an unsecured (if it is) facility, its not exactly fantastic pricing for the risk involved.

Those are some great questions! I've not thought of your last question at all so that's really fresh, thanks for sharing your insights 🙂

The most simple way i look at it is If they are willing to give you 5.25%, they must be able to earn more than 5.25% to give you the promised interest and still make a profit on the deal. As of now, i find it hard for them to generate that kind of returns given the market conditions and their decreasing financials.

That's what i tell my friends when they ask me.

InvestingWolf

Comments are closed.