4 years after I wrote about the CPF Matched Retirement Savings Scheme (MRSS), the policy has undergone further changes that anyone looking to leverage it should take note of.

Launched in January 2021, the MRSS was meant to help senior Singaporeans who have yet to hit the current Basic Retirement Sum (BRS) build their CPF retirement savings for higher monthly payouts in their retirement years. It was initially announced that MRSS would run for 5 years between 2021 – 2025, where the government will match every dollar of cash top-ups made to the Retirement Account (RA) of eligible members, up to an annual cap of $600.

I excitedly wrote back then that leveraging this scheme was a no-brainer for people who were keen to:

- Get up to $3,000 from the government (for free) during this period, and

- Enjoy tax reliefs under the Retirement Sum Topping Up (RSTU) Scheme.

We’re now in 2025; since then, our government has made further change to the policy.

The good news: You can get even MORE money now.

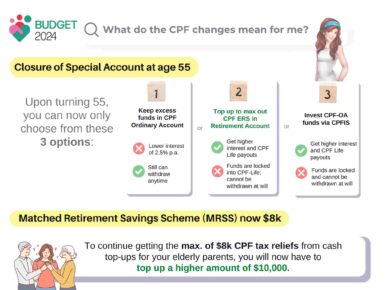

The (previously $600) annual cap has now been raised to $2,000 a year, and the age cap of 70 years old has been removed.

This means eligible seniors aged 55 years and above will now receive a dollar-for-dollar matching grant of up to this amount for cash top-ups made to their CPF Retirement Account. This has a lifetime limit of $20,000 (or approximately 10 years if you top up to the maximum each year).

This means that my father-in-law (who’s older than 70) is now eligible again (yay!), and both sides of our parents can benefit from MRSS. In total, that’s $8,000 per year that we can get in free money from the Singapore government by topping up their CPF-RA.

As my in-laws do not have substantial CPF savings during their self-employed years, we will be using this scheme to maximise and get an additional $2,000 for them every year.

The bad news: MRSS benefits will now be exempt from tax reliefs.

For the past few years, I’ve been getting the extra $600 per year from the government for 3 of my parents / in-laws while also concurrently reducing my tax liabilities. But the government has quietly taken away the tax benefit for MRSS top-ups this year.

From now on, CPF cash top-ups that attract matching grants under the MRSS will not be eligible for CPF Cash Top-up Reliefs from Year of Assessment 2026 anymore (i.e. CPF cash top-ups received from 1 January 2025).

This caught me by surprise, and if it wasn’t for the fact that I read the IRAS/CPF websites pretty often in the course of my work, I would probably have continued living under the (happy) illusion that I’m still enjoying the tax reliefs – until reality hits me next April when IRAS sends me my bill.

In the same vein, CPF cash top-ups to eligible members’ MediSave Accounts that attract the Matched MediSave Scheme (MMSS) matching grant will no longer qualify for tax reliefs anymore from YA 2027, i.e. affecting all cash top-ups made from 1 January 2026 onwards.

So yes, unfortunately this now means you will no longer be able to enjoy dual benefits from MRSS monies. In other words, your tax bill next year will not benefit from the tax reliefs unless you consciously make other moves to reduce it.

What if I still want to enjoy both MRSS and a lower tax bill?

The exempted sum is on the amount that is being given the dollar-to-dollar matching, which currently sits at a maximum of $2,000 a year per eligible senior.

On the other hand, we individuals can still enjoy tax reliefs of up to $16,000 (maximum $8,000 for self and maximum $8,000 for family members) a year for eligible CPF cash top-ups – as long as the amount does not attract MRSS and/or MMSS grants.

In other words, to continue enjoying both benefits, you will need to consider whether you might want to top up more cash.

Not everyone may need to top up to the maximum of $8,000×2 per year, as it ultimately depends on where you sit within the prevailing income tax bracket and what other moves you’ve deployed to reduce your next year’s tax bill.

For instance, let’s say you earned $80,000 this year and have already chalked up $70,000 of tax reliefs through other means:

- $48k from the Working Mother Child Relief (WMCR) benefit (for your 3 children who are above 2 years old),

- + $9k Parent Relief for your elderly dad,

- + $8k CPF cash top-up (to yourself),

- + $9k SRS top-up

Then in this case, the shortfall of $6,000 before you max out the tax relief ceiling can be achieved through topping up your parents’ CPF-RA beyond the MRSS cap. You could top up $10k for both of your parents in total, and after deducting the $2k per person that gets the dollar-for-dollar matching, the remaining $6k will be eligible for CPF cash top-up relief under the

Review your goal: Is your priority to maximise the government matching grant (MRSS/MMSS) or to maximise tax relief?

Your exact circumstances will determine whether you need to execute this move – and how much it can impact your tax bill.

Budget Babe’s take

Although removing the tax relief benefit for monies under the MRSS scheme is a huge bummer, I can understand the rationale as to why the government does not want the dual benefits to continue.

As for me, I will still be topping up all 4 of my parents CPF-RA accounts so that they get the maximum MRSS benefit from the government.

After all, free money…might as well take.

With love,

Dawn