You probably already know that your 20s are going to be the best years of your life.

Here’s another nugget of golden advice I hope someone has already told you about your 20s : it is also the best years of your life to start building wealth.

|

| No, this post is not about the book, although its cover does provide an apt summary of what I’m about to say. |

Before you get all happy and go about blowing off your first paycheck (or bonus), think about the fact that your 20s is the period of your life when you have literally no liabilities (save for your tuition fees, which you can look at repaying here). Thus, that also makes your 20s the best time for you to really build wealth and lay a foundation for early retirement.

For most of us, once we enter our 30s, we have to start thinking about wedding costs, home mortgage, raising kids, supporting our elderly parents, etc. In other words, your financial responsibilities will increase exponentially once you cross this age.

While I’ve shared a whole wealth of resources here on this blog (check out the money posts here for a start), this can easily be distilled into 2 main tips:

1. Earn like an adult, spend like a student

|

| Credits here |

The best advice I’ve adopted for myself is to earn like a professional while spending like a student. Of course, your salary as a fresh graduate probably won’t be too high in the beginning (for the record, mine was a mere $2,500 when I started) but that’s okay. Focus on building up your skills and expertise, and the monetary recognition will naturally follow once you get better at your job.

In the meantime, keep your expenditures lean. Remember when you were a poor and broke student? Economic rice was your best friend, and you could only afford the luxury of restaurant or cafe food ($12 and above) once in a fortnight. Today’s generation frequent such (what I consider to be) higher-end eateries so often just to show off their lifestyles on Instagram that it is mind-boggling, not to mention damaging on the wallet.

If you could survive on $500 back then, why can’t you do the same now? Imagine if you could maintain your spending at $600 – $800 a month, and save the rest!

The difference between your university life and your first foray into the working world is less than 2 years apart, but if your expenditure has ballooned, perhaps it is time to rethink how you survived as a student and review your spending habits. If you’re interested, I’ve previously shared some of my tips on how I trimmed my budget in order to save $20,000 on slightly more than a $30,000 annual income – that’s over 65% in savings rate.

2. Invest for an earlier retirement

Once you start saving, the next question should be – where should I best park my cash?

I’ve arranged the 5 options I recommend below in order of least effort to a little more effort needed.

To begin, the lazy man’s way would be to put your savings into accounts like OCBC 360 and UOB One which offer higher returns for your money compared to POSB or other banks.

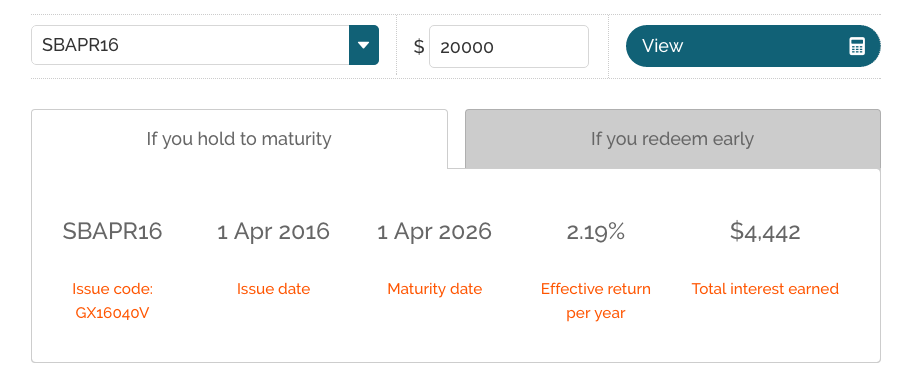

Another practically risk-free method would be to purchase the Singapore Saving Bonds – if you purchase $20,000 of SSB in April and do nothing for 10 years, you’ll be rewarded with a generous $4,442 over the same period! In simpler math, that’s a whopping 22% at the end of entire duration.

|

| Estimate your returns via the SGS website here. |

Alternatively, if you prefer greater liquidity in your cash, fixed deposits can offer attractive rates as well for a shorter holding period as compared to the SSBs. To find out who offers the best fixed deposit rates, you’ll need to research on promotional offers and actively shift your money around every few years.

If you don’t mind risk (or know how to manage your risks), two other methods could be to invest in stock market indexes or into equities.

Stock market indexes are a no-brainer – your money gets put into broad, diversified indexes that track market returns, typically comprising the largest companies on the market. In Singapore, the STI ETF is a popular option. Index investing has been touted as “automatic investing” as there’s very little homework needed before you pump your money in, and since you’re adopting a “buy and hold” strategy, you won’t have to worry too much about stock price fluctuations.

If you’re willing to work a little harder, investing in equities or stocks can be quite rewarding when you invest in the right companies who will grow and flourish over time. Generally, three types of investors appear here – income investors (who look out for dividend payouts), value investors (on the search for undervalued companies whose share price will eventually reflect its true value over time), and growth investors (trying to spot the next “big thing”).

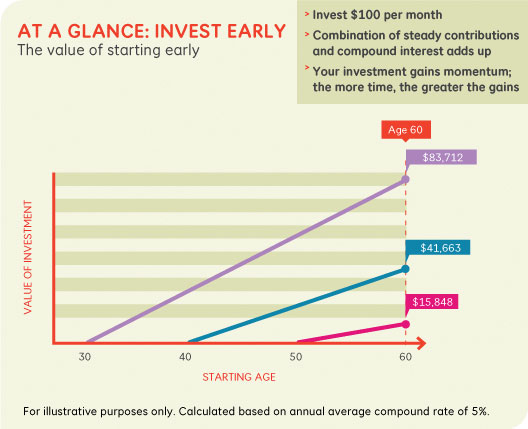

Once you start saving and investing your cash, it starts earning money all by itself. The earnings it generates will then accumulate and earn even more money, which quickly snowballs into exponential income growth! This is what they call the magic of compound interest, which grows significantly over time to reward you handsomely for your patience.

|

| Credits here |

Now, consider this: if you can save 75% of your income, you can retire in as little as 7 years! You’ve read about people retiring in their 30s or 40s, and how they did it can easily be summarized into these 2 tips, or in other words:

Earn more, spend less, invest the rest.

Don’t believe me? Look out for my next post where I crunch the numbers on how quickly you can get to retirement based on your current income (fresh grad level!) and saving rates 🙂

With love,

Budget Babe

{kind=link}

5 comments

just to ask, is there a difference between dividend investing vs index investing??

Dividend might be to buy a basket of high dividend stocks such as REITs. Index investing is to buy an exchange trading fund that tracks an index. If you want to get STI ETF, there are two of physical ETFs, get the SPDR instead of Nikko. SPDR has a lower expense ratio. Perhaps the author could explain more about physical and synthetic ETF the next time.

Lifestyle inflation was certainly a problem once I started working. It might be the stress and hours but working in an office definitely made me feel like spending more on food, drinks, travel, etc. A good post to remind myself to "earn like an adult, spend like a student"!

Cheers,

TFS

Wealth building is like what you had said simply: "Earn more, spend less, invest the rest". No shortcut here and we have to do it consistently to reap the harvest.

Sidenote, your "(check out the money posts here for a start)" link doesn't work. You may want to check again.

I am Jane from USA, It is so amazing to know such a man called Dr. Agbazara because he is so powerful that he was able to bring Dave back to me within 48 hours. Dave left for another girl and for some weeks i was so helpless because he met everything to me. But Dr. Agbazara was able to put smile in my face when he brought Dave back to me just within 48hours. And today me and Dave are back together all through the help of Dr.Agbazara whose contact details are agbazara@gmail.com OR agbazaratemple@yahoo.com

Comments are closed.