Aside from the food, blackjack and family reunions, my favourite part of Chinese New Year includes receiving my annual ang baos (red packets filled with money – a Chinese New Year tradition in Singapore). After all, who doesn’t like free money?!

With the wedding just around the corner, this year’s CNY visitations were particularly significant as it marked the last time I can get my ang baos. After we’re married, we’ll need to start giving out ang baos instead – so that means every CNY henceforth will be an immediate deficit in our wallets.

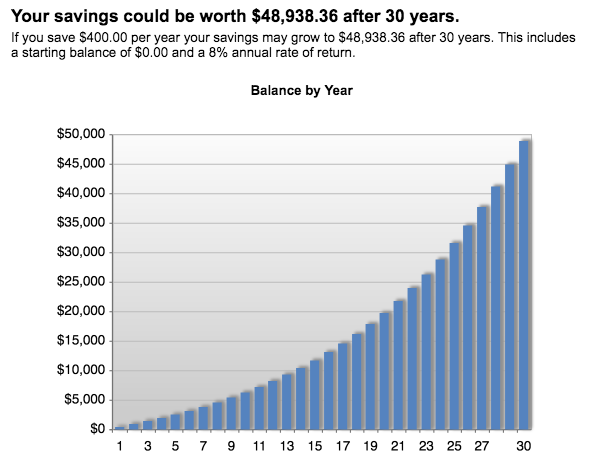

Seeing all the children get so much in ang bao money made me wonder – what if they had savvy parents who knew how to invest their money for them, so that they never had to fork out a single cent for future ang baos after they get married in the future?

|

| Photo credit: The Singapore Women’s Weekly |

Let’s imagine this scenario plays out:

|

|

Some say 8% for 30 years is too difficult. Let’s look at 5% then, which is the risk-free rate given by CPF right now. Doing such a move can still yield you 26.5 years worth of future ang baos to give out. If you top that up with your own cash, that sum can grow even further.

(Of course, most kids spend their ang bao money – although I put mine straight in the bank when I was a child, I was guilty of spending on music CDs, stickers and Enid Blyton storybooks when I was younger too.) Dang, if only my parents had done this for me.

Parents, would you consider doing this for your children?

P.S. Another way to get “free” money for your ang baos is to utilise your credit cards for maximum cashback and rebates. (I use this site to compare my credit cards before applying for any.) Store the money in a separate account and use it to partially offset your ang bao expenses every year from then on!

With love,

Budget Babe

|

18 comments

Fascinating idea!

Sort of did this for my kids. But the money goes towards building up their tertiary education fund instead. Requires further top ups monthly to build towards an $80,000 portfolio for each child by age 19.

What's left after education expenses can continue to compound for their wedding expenses and to set up a home. I doubt if there'll be much left by then though. *heh*

I think you missed out the most impt part. How to get 8% risk free?

The STI ETF's annualized returns over the past 10 years was 8.1%.

There is no instrument yielding 8% risk-free which I am aware of. Government bonds are probably the most "risk-free" you can get, and even they do not give out 8% in returns.

So your kids are the lucky ones to have you as a financially-savvy dad!

Aiya, let them pay for their own home. Actually, I paid for my own tertiary education and wedding leh. Sia la.

"Seeing all the children get so much in ang bao money made me wonder – what if they had savvy parents who knew how to invest their money for them, so that they never had to fork out a single cent for future ang baos after they get married in the future?"

Nice one! I like!

Dividend payout was only around 3% each year. The other 5% come from the appreciation of the STI ETF. Moreover, STI was at its lowest during 2008 to 2009. Unless the ETF is sold to realized the 5% appreciation. 8% cannot be achieved. If the 5% capital appreciation is not realized, it cannot be further compounded.

2014 was the last year my wife and I received hongbaos during CNY. Since 2015, we have been giving hongbaos during CNY and it's definitely a deficit in our wallets as you said. We think of it as giving our blessings to family and relatives. Hurts less!

As for investing the children's hong bao money by the parents, I reckon 8% annual rate of return applied to the addition and balance amounts in the table above is a little high. If you are applying a consistent growth rate, when can be tricky since returns can fluctuate greatly from year to year, it might be better to go with a lower annual rate of return to be applied. Maybe 5% or less?

"Let's look at 6% then, which is the risk-free rate given by CPF right now."

Are you very sure about this? Can you point me to a source on this piece of information?

"Let's look at 6% then, which is the risk-free rate given by CPF right now."

Are you very sure about this? Can you point me to a source on this piece of information?

Oops 5% sorry. Are you camping out just to catch a mistake?! You literally flag them minutes after I update. I ought to stop making changes on my mobile while at work next time- too many inaccuracies which you always flag out before I can get home to fact check.

I am keeping you accountable. Anyone with the hubris of meting out 'advice' or 'insight' should actually have the ability to be right. Otherwise, your opinions are worth zilch. If you cant handle this heat, you should probably not be a financial blogger

I am already letting it slide that even your 'revised' figure of 5% is wrong. 5% is only applicable to the first SGD 40,000 of your Special Account balance, not to CPF in general. Once again, if you want to act knowledgeable, it will help to actually be knowledgeable.

Keeping me accountable is much appreciated, although I still think there could be nicer ways of correcting me, but I guess to each his/her own.

There is a way to achieve 6%, which exists in CPF-RA for members aged 55 and above. (https://www.cpf.gov.sg/Members/AboutUs/about-us-info/cpf-interest-rates) Of course, one could argue that this isn't quite applicable for a children fund, but there are ways to go about achieving it if one thinks out of the box.

5% SA for first $40,000 is completely achievable if the parents decide to set that portion of their money aside for their children, instead of their own retirement funds. They can top up and plan their finances such that they exceed the MS, so that they can withdraw the excess in time to come, and give that to their children as a way to "return" their angpao monies.

I welcome any corrections of factual or mathematical mistakes that I might have made in the process of writing my posts, but ultimately this is still a personal blog and not a financial website proclaiming to be an expert in the field, nor am I claiming it to be an educational site. Maybe you missed out on the disclaimer I put below, which applies to every post?

"Please note that all statements published on this blog are solely opinions of my own i.e. of a personal nature, and should not in any way be taken as statements of fact. Readers are encouraged to do their own research before arriving at any conclusions based solely on materials provided, or republished, on this blog."

"Celebrated for her financially-savvy decisions, she is best known as the 24-year-old who saved $20,000 in a year upon starting her first full-time job. This $20,000 goal has since inspired an entire nation of working adults to strive for the same and get their finances in order. "

Yup, definitely not proclaiming anything 🙂 Thsnks for pointing out the disclaimer though. I think your readers should indeed be very mindful of it given the frequency with which your 'personal opinions' tend to be wrong.

Awesome post. I agree with what you mean. However, you might want to note that your angbao of $400 is before inflation so the number is actually smaller than what you can actually receive (you dont always collect $400 per year for 30 years straight either due to relatives passing away, family expanding, cousins getting married, etc…). Hence it would actually be okay to indicate an annual withdrawal of $500 from year 31 onwards to compensate for the lack of inflation influence.

In fact, it would even be okay to say that after 10 years, you effectively receive >$400 from interest earned at 8% growth without any extra deposits.

Do it for your kids! Haha. I'll be doing it for mine in the future.

Yeah agree with you, a lot of folks have been commenting that 8% is a little too high too. 4 – 6% might be better, but what's stopping us from striving for 8% if we work hard ya? 😛

I also think of all the money I gave away to my family and friends for CNY / weddings / baby shower etc as blessings. Difficult to quantify that! It is indeed a blessing to be able to give 🙂

Eh true! Should account for inflation too. I didn't factor that in as it might complicate the calculations but it is a very real consideration since the value of money has been going down over the last few decades.

Actually $400 I feel quite generous leh. I only got $100 – $200+ as a kid while growing up… haiya kids these days so blessed 😛

Comments are closed.